What Types of Properties Can Be Tokenized? Residential, Commercial, Land, and Specialized Assets Explained

This article is part of the broader Real-World Assets educational framework, examining which property categories are eligible for tokenization, what criteria determine feasibility, and how risk profiles differ across residential, commercial, industrial, hospitality, land, and specialized real estate asset classes.

Educational Notice

This article is provided for informational and educational purposes only. It does not constitute legal, financial, or investment advice. Regulatory treatment of tokenized real estate varies by jurisdiction and asset classification. Consult a qualified legal professional before engaging with any tokenized property structure.

Introduction

Understanding what types of properties can be tokenized starts with one key recognition: this technology is not restricted to a single real estate category. In principle, most legally owned property assets can be structured for tokenization, provided they meet legal, documentation, and regulatory requirements.

Tokenized real estate refers to ownership structures where legally defined economic rights are represented by blockchain-based digital tokens. But blockchain does not replace property law, corporate law, or securities regulation. The underlying property remains governed by traditional legal frameworks. The technology changes how ownership records are managed. It does not change what ownership means legally.

If you are new to the broader concept, these articles provide useful context:

- Tokenized Real Estate Explained

- Fractional Ownership in Tokenized Real Estate

- Legal Structures Behind Tokenized Real Estate

This article focuses specifically on property categories and practical examples. It does not cover the technical mechanics of tokenization in detail.

The Bank for International Settlements (BIS) consistently emphasizes that digital infrastructure enhances financial systems but does not replace the legal foundations underpinning them. That principle applies directly here: tokenization makes ownership more portable and transparent, but legal clarity must come first.

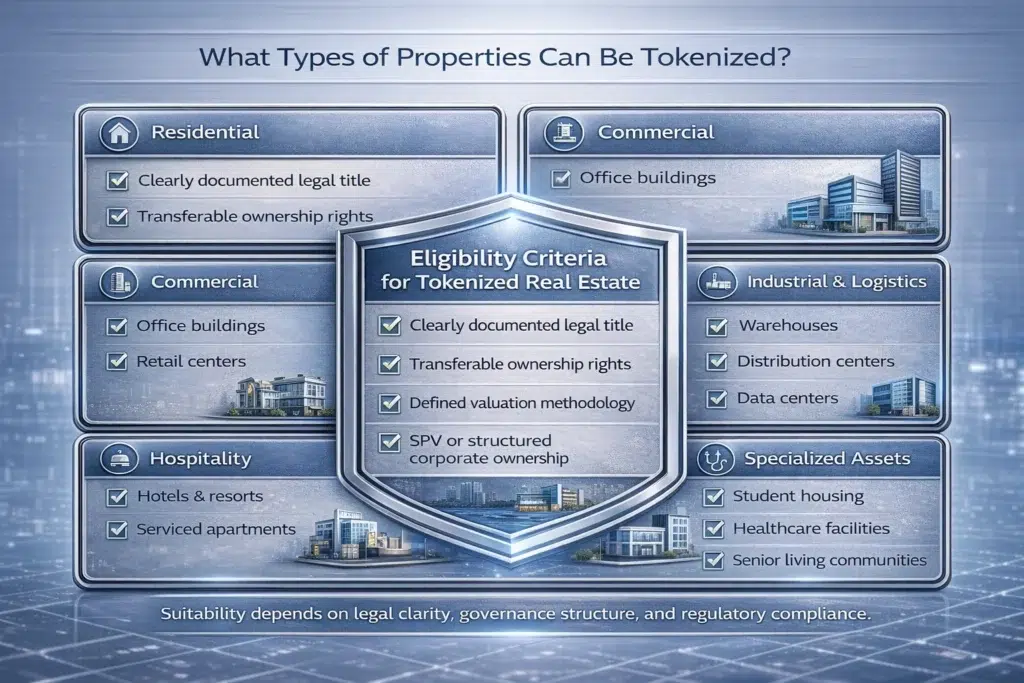

In Simple Terms: What Types of Properties Can Be Tokenized?

Most legally owned real estate assets can be tokenized if they have clear legal title (documented proof of ownership), transferable ownership rights, a defined valuation structure, and regulatory compliance. This includes residential homes, apartment buildings, commercial offices, retail centers, industrial warehouses, land parcels, hospitality properties, and specialized real estate structured under corporate entities.

The key variable is not the property type itself. It is the quality and clarity of the legal and financial documentation behind it. A warehouse with a 10-year lease and a clean SPV (Special Purpose Vehicle, a separate legal entity created to hold one asset) is far easier to tokenize than a luxury villa with disputed inheritance records.

Eligibility Criteria: What Makes a Property Tokenizable?

Before exploring categories, it helps to understand what actually determines whether a property can be tokenized. Not all real estate qualifies automatically. Eligibility depends on several conditions being met together.

A property is generally eligible if it has:

- Clearly documented legal title

- Transferable ownership rights

- A defined valuation methodology

- Proper zoning and regulatory compliance

- Structured corporate ownership, often via an SPV (Special Purpose Vehicle)

- A transparent income or development model

As explained in our guide on Legal Structures Behind Tokenized Real Estate, tokenization requires legal clarity. It does not create it. Properties with disputed ownership, incomplete documentation, or zoning uncertainty may be difficult or risky to tokenize regardless of how attractive they appear on paper.

One important principle: income-producing properties are structurally easier to tokenize than speculative ones. When a property generates regular, documented rental income, it is far simpler to model token holder returns and build transparent governance around distributions. A vacant piece of land with no income and an uncertain development timeline introduces valuation subjectivity that complicates the entire structure.

Residential Properties

Residential real estate is among the most discussed categories when evaluating what types of properties can be tokenized. The reasons are straightforward: people understand rent, leases are well-documented, and valuations follow established market methodologies. That predictability is exactly what makes residential assets attractive for token structures.

1. Single-Family Rental Homes

Single-family rental properties can be structured under a legal entity and fractionalized into tokens. They represent a familiar asset class with defined lease agreements, market-based valuations, and visible rental income. In tokenized form, the property is typically owned by an SPV. Ownership units are divided into tokens. Income distributions flow to token holders proportionally based on their holdings.

This mirrors traditional property syndication structures but introduces digital ownership records, which can simplify transfer and record-keeping. Single-family homes are often pooled together in portfolios to spread vacancy risk across multiple properties rather than concentrating it in one unit.

2. Multi-Family Apartment Buildings

Apartment complexes are often the most structurally well-suited residential assets for tokenization. They generate diversified rental income from multiple tenants. If one tenant leaves, the others continue paying. Vacancy risk is spread rather than concentrated. Multi-family buildings are frequently already held under corporate ownership, which simplifies token unitization considerably.

From a token structure perspective, apartment buildings are considered the “steady income” tier. The NOI (Net Operating Income, meaning total rental income minus all operating expenses) is relatively predictable quarter to quarter. That predictability makes it much easier to design clear distribution rules for token holders.

Commercial Real Estate

Commercial property represents a significant share of activity in tokenized real estate. The scale of assets, the institutionalization of leases, and the familiarity of commercial structures to professional investors all contribute to this.

3. Office Buildings

Office assets may be tokenized when lease agreements are clearly documented, corporate ownership is established, and tenant concentration risk (the risk that too many income streams depend on a single tenant) is manageable. Office markets have faced pressure in recent years from hybrid and remote work patterns, which means occupancy volatility is a real consideration. Careful due diligence on lease terms and tenant quality matters significantly here.

4. Retail Centers

Retail real estate includes shopping centers, strip malls, and standalone retail units. Tokenization can enable shared ownership of these assets, but risks include consumer spending sensitivity, tenant turnover, and economic downturn exposure. Retail assets require careful lease diversification analysis before tokenization. A retail center where 60% of income comes from a single anchor tenant carries a very different risk profile than one with 30 small tenants.

5. Mixed-Use Developments

Mixed-use properties combine residential, retail, and office components within a single structure or complex. They may offer diversified income streams, which can be a strength. But they also involve multiple tenant categories, complex lease structures, and sophisticated governance frameworks. Tokenizing mixed-use developments requires advanced legal structuring and careful governance design to manage the different income layers cleanly.

Industrial and Logistics Properties

Industrial real estate has gained significant prominence globally, driven largely by e-commerce growth and supply chain investment. For tokenization purposes, industrial assets have a key advantage: leases tend to be long-term and structured around corporate tenants, which creates predictable income streams.

6. Warehouses

Warehouses used for logistics and distribution are particularly well-suited for tokenization when long-term leases exist, corporate tenants are stable, and legal documentation is clear. Many warehouse leases are structured as NNN (Triple Net Leases, where the tenant pays not just rent but also property taxes, insurance, and maintenance costs). This structure leaves very clean, predictable income for the property owner, making NOI easy to model and distribute. For token holders, NNN warehouse leases represent a relatively low-management, income-predictable structure.

7. Distribution Centers

Distribution facilities serving supply chains may be suitable for tokenization, particularly when leased to established enterprises under long-term agreements. These properties are infrastructure-heavy and typically contract-based. The main risk is tenant dependency: if a single major tenant exits, income can drop sharply.

8. Data Centers

Data centers are a specialized form of real estate with long-term tenant agreements, high capital expenditure (large upfront investment in technical infrastructure), and deep operational complexity. They attract tech-focused institutional investors and are sometimes described as “Infrastructure Real Estate.” Tokenization of data centers requires robust governance frameworks due to the technical specificity of operations and the difficulty of replacing tenants quickly.

Hospitality and Short-Term Rental Properties

Hospitality assets can be tokenized, but they introduce a different kind of complexity. Unlike fixed-lease properties where income is relatively stable month to month, hospitality income is dynamic. It changes based on occupancy rates, seasonal demand, tourism patterns, and operational management quality.

9. Hotels and Resorts

Hotels present performance-based revenue: income depends on how many guests check in, not on a fixed lease. Seasonal variability and management company dependency add further layers of complexity. Tokenization of hotel assets must clearly define how revenue is distributed, how expenses are allocated, and what governance rights token holders hold over operational decisions. These are not trivial questions. A poorly designed hotel token structure can lead to disputes over revenue recognition and cost allocation.

10. Serviced Apartments and Short-Term Rentals

Short-term rental properties can be structured for tokenization under professional management frameworks. However, local licensing laws often apply, and zoning restrictions must be respected. This is a critical point: tokenization cannot override hospitality or short-term rental regulations. If a property is not legally permitted for short-term rental in its jurisdiction, putting it into a token structure does not change that. The zoning law governs the physical property regardless of how ownership is recorded.

Land and Development Projects

Land and development projects introduce additional complexity compared to income-producing properties. The core challenge is that land alone often generates no income while still requiring legal maintenance, property taxes, and governance. This makes valuation subjective and token holder distributions difficult to define.

11. Raw Land

Raw land can be tokenized if legal title is clear, zoning is defined, and ownership is transferable. However, raw land typically produces no income. Risks include illiquidity (difficulty selling quickly at fair value), development uncertainty, and valuation subjectivity. Raw land tokens are closer to a speculative bet on future development or appreciation than an income-producing investment structure.

12. Development Projects

Development projects may be structured for tokenization, with capital raised for construction, milestone-based funding releases, and future income projections built into the token terms. This type of tokenization may resemble securities offerings and can trigger regulatory oversight from bodies such as the U.S. Securities and Exchange Commission (SEC) or the European Securities and Markets Authority (ESMA). Regulatory classification depends heavily on how returns are promised and how much investor control exists over the development process.

As explained in Real-World Asset Tokenization Explained, the legal structure of any tokenization always determines what regulatory framework applies.

13. Agricultural Land

Farmland may be tokenized when ownership documentation is clear, lease income structures are defined, and regulatory compliance is maintained. Agricultural assets introduce environmental and seasonal variability that affects income predictability. Lease-based farmland, where a farmer pays annual rent for use of the land, is structurally easier to tokenize than speculative undeveloped agricultural plots.

Specialized Real Estate Assets

Beyond the main categories, several niche property types may also be structured for tokenization. Each brings specific lease, regulatory, or operational considerations that must be addressed carefully in the governance design.

14. Student Housing

Purpose-built student accommodation can be structured under fractional ownership models. Key considerations include academic-year leasing cycles, which create predictable but short-term income patterns, and seasonal vacancy during summer months. Student housing often benefits from proximity to universities and strong, recurring demand. Governance must account for the high tenant turnover inherent in the sector.

15. Healthcare Facilities

Healthcare real estate, including medical clinics, outpatient centers, and specialist facilities, can be tokenized when lease contracts are clearly defined and regulatory compliance is maintained. Healthcare assets involve sector-specific oversight from health authorities in addition to standard property regulations. Tenant stability in healthcare can be very strong, since healthcare operators rarely relocate, making these assets attractive for long-term income structures.

16. Senior Living Communities

Senior housing may generate stable, long-term income, but it involves complex operational management and healthcare regulation considerations. Governance documentation must be detailed and clear, covering how operational decisions are made, how costs are allocated, and what oversight mechanisms exist for the care services provided. These assets require more governance depth than a simple commercial lease structure.

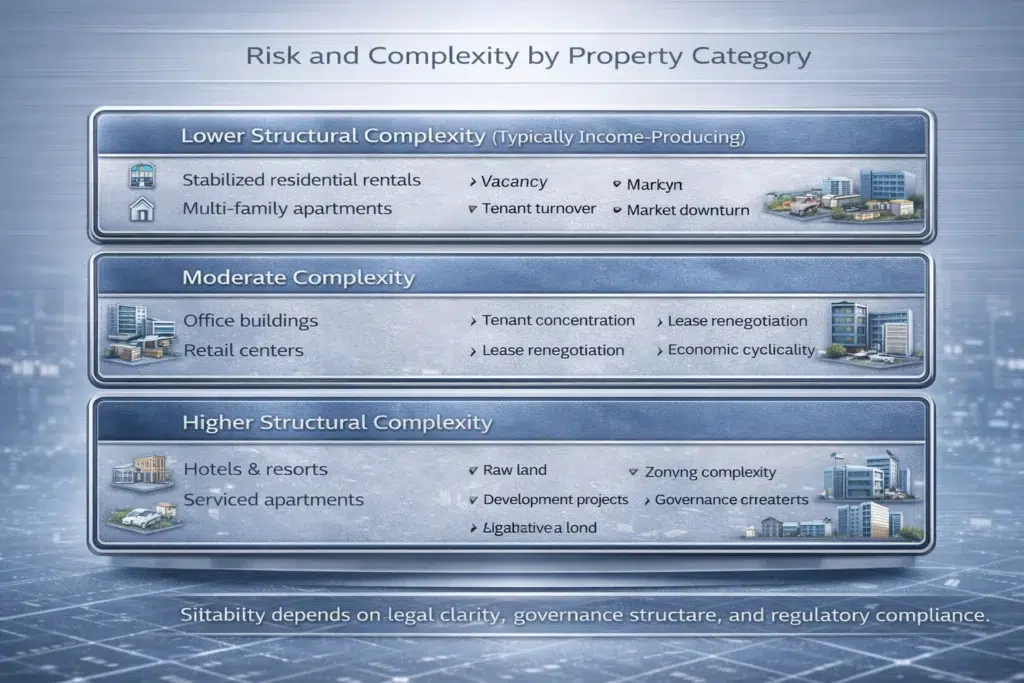

Which Properties Are More Complex to Tokenize?

Not all property types are equally suited to tokenization. Some categories introduce structural challenges that make the process significantly more complex, regardless of how attractive the underlying asset may appear.

Higher complexity typically arises with:

- Assets with unclear title history or disputed ownership

- Cross-border ownership structures involving multiple legal systems

- Heavily regulated sectors such as healthcare or hospitality

- Performance-based revenue assets where income is dynamic rather than fixed

- Early-stage development projects with no existing income

Income-producing properties with clear, long-term lease agreements are generally the easiest to structure. The more predictable the NOI (Net Operating Income), the simpler the token distribution model can be.

Why Institutional Platforms Prioritize Certain Property Types

Institutional-grade tokenization platforms tend to focus on a specific subset of real estate categories. This is not arbitrary. It reflects a clear preference for assets that combine income predictability, legal clarity, and governance simplicity.

Institutional platforms typically prioritize:

- Stabilized income-producing assets with documented rental history

- Clean SPV ownership structures holding a single asset

- Transparent lease documentation, ideally with NNN (Triple Net Lease) terms

- Jurisdictional regulatory clarity with no cross-border ambiguity

- Strong governance frameworks defining token holder rights clearly

There is also an operational reality that platforms must acknowledge: blockchain does not fix a leaky roof. Property management remains a human requirement. A qualified property manager, a asset servicer, or a PropTech (property technology) management platform must still handle day-to-day operational decisions. Token structures govern ownership and income distribution. They do not govern maintenance, tenant relations, or physical upkeep.

This is why the “Expert Check” before tokenizing any property involves three non-negotiable questions. First, who is the property manager? Second, is the SPV clean, meaning it holds only one asset so that risk is isolated? Third, what is the actual NOI after all operating expenses are deducted? Total rent figures are not the relevant number. Net Operating Income is what matters for token holder returns.

As the Bank for International Settlements (BIS) consistently emphasizes, digital infrastructure enhances financial systems but cannot replace the legal and operational foundations beneath them. Legal clarity determines feasibility. Operational quality determines sustainability.

For broader context on how tokenized real estate interacts with investment frameworks, see Benefits and Risks of RWA Tokenization.

Property Type Summary: Predictability, Income, and Complexity

| Property Type | Income Style | Management Level | Complexity | Best Suited For |

|---|---|---|---|---|

| Apartments (Multi-Family) | Steady / Monthly | Professional | Low | Long-term income structures |

| Warehouses / Industrial | High / Long-term | Low (tenant pays costs) | Low to Medium | Institutional investors |

| Office Buildings | Lease-based | Medium | Medium | Established commercial markets |

| Hotels / Hospitality | Dynamic / Seasonal | High (operational) | High | Yield seekers with risk tolerance |

| Raw Land | None (capital gain) | Minimal | High | Speculative structures only |

| Development Projects | Future / Milestone | High | Very High | Experienced capital structures |

| Student Housing | Seasonal / Annual | Medium | Medium | Niche income strategies |

| Healthcare / Senior Living | Long-term lease | High (regulated) | High | Specialized governance platforms |

Risks by Property Category

Even when a property is successfully tokenized, the underlying risks of that asset class do not disappear. Tokenization modernizes ownership records. It does not eliminate property-level risk. Understanding risk by category is essential before evaluating any tokenized real estate structure.

Residential Risks

- Vacancy periods with no rental income

- Tenant turnover and re-leasing costs

- Maintenance and unexpected repair expenses

Commercial Risks

- Lease renegotiation at renewal, often at lower rates in weak markets

- Economic sensitivity affecting tenant revenues and ability to pay

- Tenant concentration, where too much income depends on one or two tenants

Industrial Risks

- Tenant dependency on a single large corporate lessee

- Supply chain shifts reducing demand for specific logistics locations

Land Risks

- Illiquidity, meaning the asset is difficult to sell quickly at fair value

- Zoning change risk affecting permitted use

- Development uncertainty, particularly for early-stage projects

Hospitality Risks

- Revenue volatility based on occupancy rates and seasonal patterns

- Tourism and travel demand exposure

- High operational management costs reducing NOI (Net Operating Income)

Understanding risk is part of understanding what types of properties can be tokenized at a structural level. The right question is not just “can this be tokenized” but “should this be tokenized, and under what governance framework?” For a broader view of how risk factors apply across tokenized assets, see Benefits and Risks of RWA Tokenization and How Investors Assess Risk in Tokenized Real-World Assets.

For infrastructure and governance mechanisms that support accountability in these structures, see What Is Proof of Reserve and On-Chain Transparency Explained.

FAQ: What Types of Properties Can Be Tokenized?

Can any property be tokenized?

No. The property must have clear legal title (documented proof of ownership), transferable ownership rights, and regulatory compliance. Properties with disputed ownership, incomplete documentation, or unresolved zoning issues are generally not suitable for tokenization regardless of asset type.

Can you tokenize your own home?

In principle, yes, if the property is structured legally under an entity such as an SPV (Special Purpose Vehicle) and the structure complies with applicable securities regulations. However, this is not a simple process and requires qualified legal advice specific to your jurisdiction.

Can land be tokenized?

Yes, but land without income typically carries higher valuation and liquidity risk than income-producing properties. Raw land tokens are closer to speculative structures than income-distribution structures. Tokenizing land is possible, but the absence of NOI (Net Operating Income) makes governance design and token holder returns significantly harder to define.

Are rental properties easier to tokenize than development projects?

Generally yes. Income-producing rental properties with documented leases are structurally simpler to tokenize than speculative development projects. The predictability of rental income makes token distribution rules much clearer. Development projects introduce construction risk, timeline uncertainty, and often require regulatory classification as securities offerings.

Is commercial property better suited for tokenization than residential?

Not necessarily better, but structurally different. Commercial assets with NNN (Triple Net Lease) agreements offer very clean income structures with low management overhead, which suits institutional token platforms. Residential assets offer broader market familiarity and diversification through multi-family portfolios. Suitability depends on governance design, investor profile, and regulatory context.

Does tokenization change zoning laws or local regulations?

No. Tokenization records ownership on a blockchain. It has no effect on zoning laws, local licensing requirements, or hospitality regulations. A property that is not legally permitted for short-term rental in its jurisdiction remains subject to those restrictions regardless of how its ownership is structured digitally.

Conclusion

Understanding what types of properties can be tokenized reveals that tokenization is not limited to one real estate category. Residential homes, apartment complexes, office buildings, retail centers, warehouses, land parcels, hospitality assets, agricultural properties, and specialized facilities may all be structured for tokenization, provided legal clarity and regulatory compliance are established.

But the category of the property is only one part of the picture. Legal structure determines feasibility. Regulatory compliance determines validity. Governance design determines sustainability. And operational management, always human and always necessary, determines whether token holder returns are actually delivered.

The properties that work best in token structures share common traits: clear income, clean legal ownership, transparent governance, and qualified management. The further a property moves from those traits, the more complex and risky the tokenization becomes.

Tokenization modernizes ownership infrastructure. The underlying property remains governed by the same laws, managed by the same humans, and subject to the same market forces it always was.

Sources and Regulatory References

- Bank for International Settlements (BIS): https://www.bis.org

- U.S. Securities and Exchange Commission (SEC): https://www.sec.gov

- European Securities and Markets Authority (ESMA): https://www.esma.europa.eu

Educational Disclaimer

This article is provided for educational purposes only and does not constitute financial, legal, or investment advice. Regulatory treatment of tokenized real estate varies by jurisdiction and asset classification. Professional legal consultation should be obtained before engaging with any tokenized property structure.

Last updated: March 2026

Explore Tokenized Real Estate

- Tokenized Real Estate Explained

- Fractional Ownership in Tokenized Real Estate

- Legal Structures Behind Tokenized Real Estate

- How Tokenized Real Estate Works Compared to Traditional Property Investment

- Benefits and Risks of Tokenized Real Estate

- Benefits and Risks of RWA Tokenization (cluster)

- Real-World Asset Tokenization Explained (cluster)

- On-Chain Transparency Explained (cross-pillar)

- What Is Proof of Reserve (cross-pillar)

- Real-World Assets Hub

{kind=link}