Legal Structures Behind Tokenized Real Estate: SPVs, Securities Law, and Regulatory Compliance Explained

This article is part of the broader Real-World Assets educational framework, examining how tokenized real estate is enforced by law, what legal entity structures are used, how securities regulation applies, and what due diligence questions every investor should ask before engaging with a tokenized property structure.

Educational Notice

This article is provided for informational and educational purposes only. It does not constitute legal, financial, or investment advice. Regulatory treatment of tokenized real estate varies significantly by jurisdiction and structure. Consult a qualified legal professional before establishing or interacting with any tokenized property arrangement.

Introduction

Understanding the legal structures behind tokenized real estate is essential for evaluating enforceability, investor protection, and regulatory compliance. Many people assume a real estate token is simply a digital file. In practice, a token is more like a digital key that unlocks a defined set of real-world legal rights. Without a solid legal structure underneath it, that key opens nothing. With the right structure in place, it represents a legally enforceable asset.

Tokenized real estate refers to ownership structures where legally defined economic rights tied to property assets are represented by blockchain-based digital tokens. But blockchain technology does not replace property law, corporate law, or securities regulation. The legal structure, not the blockchain, ultimately determines ownership rights, governance authority, and enforceability.

If you are new to tokenized property models, these articles provide useful context:

- Tokenized Real Estate Explained

- How Tokenized Real Estate Works Compared to Traditional Property Investment

- Fractional Ownership in Tokenized Real Estate

- Benefits and Risks of Tokenized Real Estate

This article explains the core legal structures behind tokenized real estate, how securities law applies, the role of property registries, governance frameworks, AML (Anti-Money Laundering) and KYC (Know Your Customer) compliance, custody considerations, and cross-border regulatory complexity.

The Bank for International Settlements (BIS) consistently emphasizes that distributed ledger technologies enhance financial infrastructure but do not replace legal institutions. Any credible tokenized real estate structure must anchor ownership within recognized legal frameworks, not merely on a blockchain ledger.

In Simple Terms: What Are the Legal Structures Behind Tokenized Real Estate?

The legal structures behind tokenized real estate typically involve Special Purpose Vehicles (SPVs, separate legal entities created to hold a single asset), limited liability companies (LLCs), partnerships, or corporate entities that hold legal title to property. Digital tokens represent ownership units in these entities. Courts enforce rights based on property and corporate law, not on blockchain records.

There is also an important distinction that many first-time investors miss: most real estate tokens offer Rights to Income (a share of rental distributions or sale proceeds) but not Rights of Possession (you cannot physically occupy or use the property based on token ownership alone). The token represents a financial interest in the legal entity that owns the property. Understanding that distinction is fundamental to understanding what you actually hold.

Why Legal Architecture Matters in Tokenized Real Estate

When analyzing the legal structures behind tokenized real estate, one principle stands above all others: blockchain records ownership representation, but courts enforce ownership based on legal documentation. The two systems serve different functions. They must work together, not substitute for each other.

Key legal foundations include:

- Legal title recorded in official land registries (government property records)

- Corporate documentation defining investor rights and governance rules

- Securities law potentially governing how tokens are issued and sold

- Regulatory compliance determining the validity and enforceability of the structure

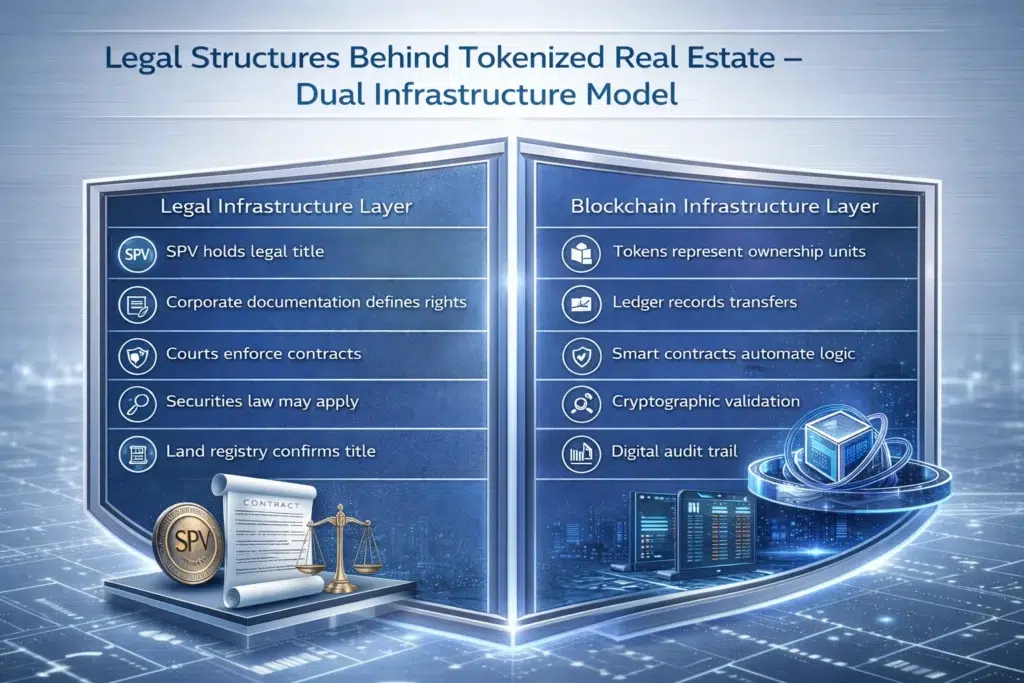

Legal Layer vs Blockchain Layer in Tokenized Real Estate

Understanding the legal structures behind tokenized real estate requires separating two coordinated systems that work in parallel. Neither replaces the other. Each handles a different dimension of ownership.

| Legal Infrastructure Layer | Blockchain Infrastructure Layer |

|---|---|

| SPV holds legal property title | Tokens represent ownership units in the SPV |

| Courts enforce contractual rights | Ledger records transfers between token holders |

| Securities law may apply to token issuance | Smart contracts automate distribution logic |

| Land registries confirm legal title | Cryptographic validation confirms transactions |

| Determines enforceability | Improves record efficiency and transparency |

The blockchain layer makes ownership more portable and transparent. The legal layer makes it enforceable. Both are necessary. Neither is sufficient on its own.

Core Legal Entity Structures Used in Tokenized Real Estate

1. Special Purpose Vehicle (SPV): The Safe Box of Real Estate

The SPV (Special Purpose Vehicle, a separate legal entity created specifically to hold one asset) is the most common and most important structure within tokenized real estate. Think of it as a locked safe box built around a single property. The property sits inside that box. Token holders own shares of the box. And critically, if the tokenization platform or developer faces financial difficulties, the box remains intact.

This protection is called Bankruptcy Remoteness (also known as Ring-Fencing), meaning the property asset held inside the SPV is legally isolated from the debts and liabilities of the platform operating around it. If the company running the tokenization platform goes bankrupt, the SPV and its property are not part of the insolvency estate. Investor interests are protected because their asset is legally separated.

How the SPV structure works in practice:

- An SPV is incorporated as a separate legal entity in a recognized jurisdiction

- The SPV holds legal title to the property, recorded in the official land registry

- Ownership interests in the SPV are divided into defined units

- Digital tokens represent those ownership units on the blockchain

Why institutional platforms use SPVs:

- Isolate liability to a single property, protecting investors from unrelated risks

- Provide legal clarity of ownership through corporate documentation

- Enable fractional participation without changing the underlying title structure

- Define governance rules contractually in the SPV’s operating agreement

SPVs are typically structured as limited liability companies, corporations, or limited partnerships, depending on the jurisdiction and the investor profile being targeted. The validity of tokenized ownership depends entirely on how clearly tokens are linked to SPV equity or contractual rights in the governing documents.

It is also worth noting that the smart contract acts as the bridge between the two registries: it automatically updates the digital ledger when tokens transfer while remaining anchored to the land registry’s master title held by the SPV. The smart contract audit process verifies that this bridge functions as documented.

2. Limited Liability Company (LLC)

In the United States and several other jurisdictions, LLCs (Limited Liability Companies, corporate entities that combine flexible governance with limited personal liability for members) are frequently used as the legal wrapper in tokenized real estate structures. Their operating agreements can define investor rights, income distribution rules, voting procedures, and exit mechanisms in considerable detail.

Tokens may represent membership interests in the LLC. If those tokenized membership interests meet regulatory thresholds under US securities law, the U.S. Securities and Exchange Commission (SEC) may classify them as securities, triggering registration or exemption requirements. Platforms operating under compliant frameworks typically use specific exemptions. Regulation D (for accredited, typically high-net-worth investors in the US), Regulation S (for investors located outside the United States), and Regulation A+ (a lighter exemption allowing broader retail participation up to certain capital limits) are the most common pathways used in institutional-grade tokenized real estate offerings.

3. Limited Partnership (LP)

Limited partnerships are common in traditional real estate syndications and are sometimes adapted to tokenized structures. The General Partner (GP) manages the property and carries operational responsibility. The Limited Partners (LPs) provide capital and receive income distributions while holding limited personal liability. Tokens may represent limited partnership interests, giving holders economic rights without direct management control.

LP structures provide governance clarity but require careful compliance with both partnership law and securities regulation, particularly when interests are offered to multiple investors across different jurisdictions.

4. Corporate Share Structures

In some tokenization models, a corporation owns the property, shares represent ownership interests, and tokens digitally represent those shares on the blockchain. Corporate governance rules then determine voting rights, dividend distribution procedures, sale processes, and director authority. Corporate law governs enforceability. This structure is familiar to institutional investors and can integrate with existing regulatory frameworks in many jurisdictions, including the EU’s DLT Pilot Regime (European Union framework for experimenting with blockchain-based securities settlement under regulatory oversight).

Securities Law Considerations in Tokenized Real Estate

One of the most significant aspects of legal structures behind tokenized real estate is securities classification. Getting this wrong is not a grey area. It is a regulatory compliance failure with serious consequences.

When Tokenized Real Estate May Be Considered a Security

Tokenized interests may fall under securities regulation when they involve an investment of capital in a common enterprise, with an expectation of profit derived from the managerial efforts of others. In the US, this is evaluated under the Howey Test (the legal standard applied by the SEC to determine whether a transaction constitutes an investment contract). If a token passes this test, it is a security and must be registered or issued under a recognized exemption.

In the European Union, the European Securities and Markets Authority (ESMA) provides oversight for securities offerings. In the UAE, VARA (Virtual Assets Regulatory Authority) governs virtual asset activities. Securities classification may trigger registration requirements, disclosure obligations, investor eligibility rules, and ongoing reporting duties. Failure to align with applicable securities law creates significant regulatory exposure regardless of how the structure is labelled.

Property Law and Land Registry Considerations

Regardless of tokenization, property law remains central. Legal title must be recorded in official land registries (government-administered databases recording property ownership). Token ownership does not replace deed registration. Courts enforce ownership based on statutory property records, not blockchain entries. Land registry systems are administered by national or regional authorities, and blockchain records have no authority to override them.

The legal structures behind tokenized real estate must clearly document the linkage between tokens and legally recognized ownership rights. Without that documented chain connecting the token to the SPV equity to the land registry title, the token’s enforceability is uncertain.

Custody Considerations in Tokenized Real Estate

Legal structures behind tokenized real estate involve two distinct forms of custody that must both be addressed.

Property custody refers to the SPV holding legal title, with property management agreements defining operational duties and title documentation maintained securely. Digital asset custody refers to how the tokens themselves are stored and controlled: access controls must be defined, cybersecurity safeguards applied, and the token custody infrastructure maintained reliably. Digital custody introduces operational considerations that have no equivalent in traditional deed ownership.

For context on how verification mechanisms support custody integrity, see What Is Proof of Reserve and On-Chain Transparency Explained.

Governance and Investor Rights

Governance frameworks define what token holders can actually do and receive. This includes voting rights on major decisions, income distribution procedures, property sale processes, conflict resolution mechanisms, and procedures for removing or replacing the manager. These provisions are codified in operating agreements, shareholder agreements, partnership agreements, and subscription documents. The blockchain records holdings. The legal documentation defines what those holdings mean in practice.

The distinction between Rights to Income and Rights of Possession is critical here. Most tokenized real estate structures grant token holders a proportional right to rental income distributions and sale proceeds. They do not grant any right to physically occupy or use the property. Governance documents must make this distinction explicit to avoid investor confusion and potential disputes.

AML, KYC, and Regulatory Compliance

Tokenized real estate platforms are typically subject to AML (Anti-Money Laundering, laws requiring financial platforms to detect and prevent money laundering) and KYC (Know Your Customer, identity verification requirements for all investors) obligations, reporting duties, and investor accreditation rules.

In practice, this means investor wallets must be whitelisted before they can hold or receive tokens. The whitelisting process is often managed through Identity Oracles (automated verification systems connected to smart contracts that check KYC and AML status before permitting a wallet to hold tokens). Only verified, approved wallets can participate. This is not optional architecture for investment platforms. It is a regulatory requirement in most jurisdictions where tokenized securities are offered.

Tokenized real estate platforms may specifically be subject to:

- AML laws requiring transaction monitoring and suspicious activity reporting

- KYC requirements verifying investor identity before onboarding

- Ongoing reporting obligations to regulatory authorities

- Investor accreditation rules restricting participation to eligible investors

Cross-Jurisdictional Complexity

The legal structures behind tokenized real estate often involve cross-border considerations that add significant complexity. Tokenized property platforms frequently attract investors from multiple countries, hold assets in one jurisdiction, and incorporate their legal entities in another. This creates layered regulatory exposure that no single compliance framework fully resolves on its own.

Complexities that commonly arise include differing securities classifications across jurisdictions, divergent property law systems, different tax treatment for token income, investor eligibility restrictions varying by country, and the practical challenge of cross-border legal enforcement. Legal enforceability depends on where the property is located, where the issuing entity is incorporated, and where investors reside. Cross-border tokenization requires coordinated legal design that anticipates all three dimensions from the outset.

For regulatory frameworks that address cross-border digital asset activity, see What Is MiCA Regulation and What Is VARA Regulation.

Why Institutional Investors Prioritize Legal Structure

Institutional capital does not enter structures where enforceability is uncertain. Institutional participants focus on legal enforceability, regulatory clarity, governance transparency, auditability of ownership records, and jurisdictional stability. Tokenized real estate without a robust legal foundation lacks institutional credibility regardless of how sophisticated its blockchain infrastructure may be.

This is why platforms targeting institutional capital invest heavily in legal structuring before building any technology. The legal architecture is the product. The blockchain is the delivery mechanism.

For broader context on how compliance and governance interact with real estate tokenization, see Why Compliance Matters in Tokenized Finance.

Common Legal Risks in Tokenized Real Estate

Understanding the legal structures behind tokenized real estate requires acknowledging where things can go wrong. Several categories of legal risk are particularly common in this space.

Misclassification Risk arises when tokens are issued without determining whether they constitute securities. If they do and no exemption applies, the issuance may be illegal. Governance Weakness occurs when investor rights are vaguely defined in operating documents, creating disputes about income distribution or decision-making authority. Documentation Gaps happen when the chain linking tokens to SPV equity to land registry title is incomplete or ambiguous, undermining enforceability. Cross-Border Enforcement Risk appears when jurisdictional differences make it difficult to obtain legal remedies. Regulatory Change Risk is the ongoing exposure created by evolving digital asset laws that may affect compliance obligations retroactively. Legal clarity mitigates all five of these risks. Incomplete legal structuring does not.

Due Diligence: 5 Questions Every Investor Should Ask

Before evaluating any tokenized real estate structure, a clear set of due diligence questions should be answered. The table below sets out the five most important questions, why each matters, and what an authoritative answer looks like.

| Question | Why It Matters | What an Authoritative Answer Looks Like |

|---|---|---|

| Is the property held in an SPV? | Asset protection via Bankruptcy Remoteness | Yes, each property is held in its own isolated legal entity |

| What rights do tokens represent? | Knowing exactly what you own: income rights vs possession rights | Rights to rental income distributions and capital gain proceeds, not physical possession |

| Is KYC mandatory for token holders? | Legal compliance with AML and securities law | Yes, only whitelisted wallets verified through Identity Oracles can hold tokens |

| Is there an independent trustee or custodian? | Third-party oversight of SPV assets and token custody | A licensed third-party firm independently oversees SPV assets and digital custody |

| Where is the entity registered? | Jurisdictional safety and regulatory clarity | Registered in a recognized regulatory jurisdiction such as Dubai under VARA, the EU under MiCA, or the US under SEC exemptions |

FAQ: Legal Structures Behind Tokenized Real Estate

Is tokenized real estate legal?

Tokenized real estate can be legal if structured within applicable property law and securities regulation frameworks. Legal status depends on the jurisdiction, the entity structure used, how tokens are classified, and whether the platform has obtained required authorizations or exemptions.

Are tokenized property tokens considered securities?

In many jurisdictions, yes. If the token represents an investment in a common enterprise with an expectation of profit from others’ efforts, it will likely be classified as a security under tests such as the US Howey Test. Compliant platforms use recognized exemptions such as Regulation D, Regulation S, or Regulation A+ to issue tokens legally.

Who legally owns the property in a tokenized structure?

Typically, a legally incorporated SPV holds the property title. Token holders hold ownership interests in that SPV entity. The SPV is the legal owner recognized by the land registry. Token holders hold financial interests in the SPV, not direct title to the property itself.

Does blockchain replace land registries?

No. Official land registries remain the authoritative record of property ownership under property law. Blockchain records the token ownership layer, which represents interests in the legal entity that holds the title. The two systems work together. Neither replaces the other.

What is Bankruptcy Remoteness and why does it matter?

Bankruptcy Remoteness means the property asset held inside the SPV is legally isolated from the debts and liabilities of the platform company operating around it. If the platform goes bankrupt, the SPV and its property are not part of the insolvency estate. This protection is the primary reason institutional-grade tokenization uses individual SPVs per property rather than pooling assets into a single entity.

What is the difference between Rights to Income and Rights of Possession?

Rights to Income means token holders receive a proportional share of rental distributions and sale proceeds. Rights of Possession would mean token holders can physically occupy or use the property. Most tokenized real estate structures grant only the former. Token holders are financial investors, not occupants. Governance documents must make this explicit.

Conclusion

Understanding the legal structures behind tokenized real estate is fundamental to evaluating enforceability, compliance, and investor protection. Blockchain makes real estate ownership more portable and transparent. The legal structure makes it safe and enforceable.

Tokenized real estate typically relies on SPV-based entity structures with Bankruptcy Remoteness protection, corporate governance frameworks defining investor rights clearly, securities law compliance through recognized exemptions, official land registry registration, AML and KYC procedures including Identity Oracle whitelisting, and robust digital custody safeguards.

Legal structure determines validity. Regulatory compliance determines sustainability. Governance clarity protects investors. Institutional-grade tokenization requires careful coordination between technology and law, with the legal architecture treated as the foundation rather than an afterthought.

For related reading: Real-World Asset Tokenization Explained, Why Compliance Matters in Tokenized Finance, and Who Verifies Real-World Assets in Tokenized Systems.

Sources and Regulatory References

- Bank for International Settlements (BIS): https://www.bis.org

- U.S. Securities and Exchange Commission (SEC): https://www.sec.gov

- European Securities and Markets Authority (ESMA): https://www.esma.europa.eu

Educational Disclaimer

This article is provided for educational purposes only and does not constitute legal, financial, or investment advice. Regulatory treatment of tokenized real estate varies by jurisdiction and asset classification. Professional legal consultation should be obtained before engaging with any tokenized property structure.

Last updated: March 2026

Explore Tokenized Real Estate Legal Frameworks

- Tokenized Real Estate Explained

- Fractional Ownership in Tokenized Real Estate

- How Tokenized Real Estate Works Compared to Traditional Property Investment

- Benefits and Risks of Tokenized Real Estate

- What Types of Properties Can Be Tokenized

- Benefits and Risks of RWA Tokenization (cluster)

- Why Compliance Matters in Tokenized Finance (cross-pillar)

- What Is MiCA Regulation (cross-pillar)

- On-Chain Transparency Explained (cross-pillar)

- Real-World Assets Hub

{kind=link}