How Tokenized Real Estate Works Compared to Traditional Property Investment: Legal, Liquidity, and Structural Differences Explained

This article is part of the broader Real-World Assets educational framework, providing a structured, symmetric comparison of how tokenized real estate works compared to traditional property investment across legal architecture, capital requirements, liquidity mechanics, operational infrastructure, and risk exposure.

Educational Notice

This article is provided for informational and educational purposes only. It does not constitute financial, legal, or investment advice. Regulatory treatment of tokenized real estate varies by jurisdiction and asset classification. This guide is educational and neutral in tone and does not promote any investment strategy.

Introduction

The dream of owning real estate has always been about two things: rental income and capital appreciation. But the way investors access those returns is splitting into two distinct models. The traditional model is built on direct legal title, meaning your name is on the deed recorded in a government land registry and enforced through established property and contract law. The tokenized model introduces a blockchain-based digital ownership layer representing structured economic rights tied to legally owned property assets held inside a legal entity.

This is not simply old versus new. These two models make fundamentally different trade-offs. Traditional direct-title ownership offers Zero Counterparty Risk (meaning no company’s bankruptcy can affect your legal title once you hold the deed). Tokenized ownership offers Maximum Efficiency: lower entry thresholds, programmable income distribution, potential 24/7 transferability, and Real-Time NAV (Net Asset Value, the current market value of the underlying property reflected in the token price).

Understanding how tokenized real estate works compared to traditional property investment requires examining both models honestly, without dismissing the unique value of either.

If you are new to real-world assets, begin here:

- What Are Real-World Assets?

- Tokenized Real Estate Explained

- Fractional Ownership in Tokenized Real Estate

The Bank for International Settlements (BIS) has emphasized that distributed ledger technologies (shared databases maintained simultaneously across multiple participants) enhance financial infrastructure but do not replace legal systems. Both models operate within enforceable legal frameworks. They differ in how that legal framework is structured, accessed, and administered.

In Simple Terms: How Does Tokenized Real Estate Work Compared to Traditional Property Investment?

Traditional property investment involves direct legal ownership recorded in government land registries. Your name is on the deed. Courts enforce that right directly.

Tokenized real estate works by dividing structured property ownership, typically held inside an SPV (Special Purpose Vehicle, a separate legal entity created to hold one asset), into blockchain-based digital tokens representing fractional economic rights. Token holders do not own the building directly. They hold Allocated interests (specific, identifiable economic rights in a specific property through a defined legal entity) rather than Unallocated interests (general claims against a pool with no specific asset backing). Institutional-grade tokenized structures are always Allocated.

Both rely on enforceable legal systems. They differ in capital access, transfer processes, liquidity structure, and operational infrastructure.

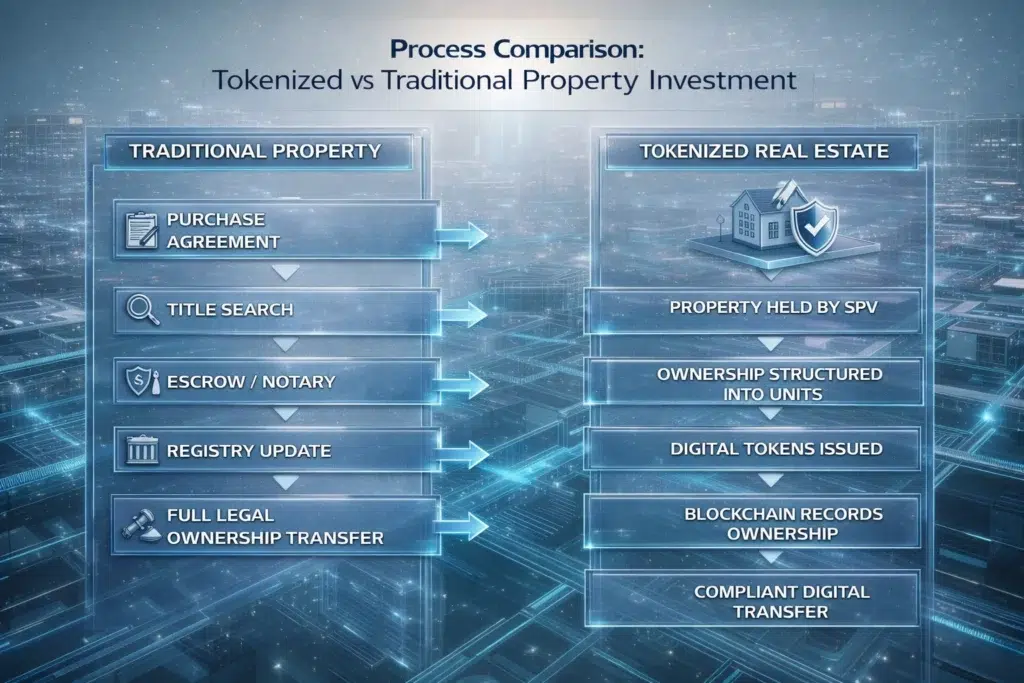

Process Overview: How Each Model Works Step by Step

Traditional Property Investment

- Buyer and seller execute a purchase agreement

- Title search confirms clean ownership history

- Escrow (third-party holding of funds during the transaction) or notary process manages the exchange

- Land registry is updated to reflect the new owner

- Full legal ownership transfers directly to the buyer

Tokenized Real Estate

- Property is legally transferred to and held by a legal entity (usually an SPV)

- Ownership of the SPV is divided into defined, structured units

- Digital tokens are issued representing those units on a blockchain

- Blockchain records token ownership and transfer history

- Transfers occur via compliant digital infrastructure with programmable compliance checks

Legal Structure Differences

Understanding how tokenized real estate works compared to traditional property investment begins with legal architecture, because legal architecture determines what you actually own and what protections you have.

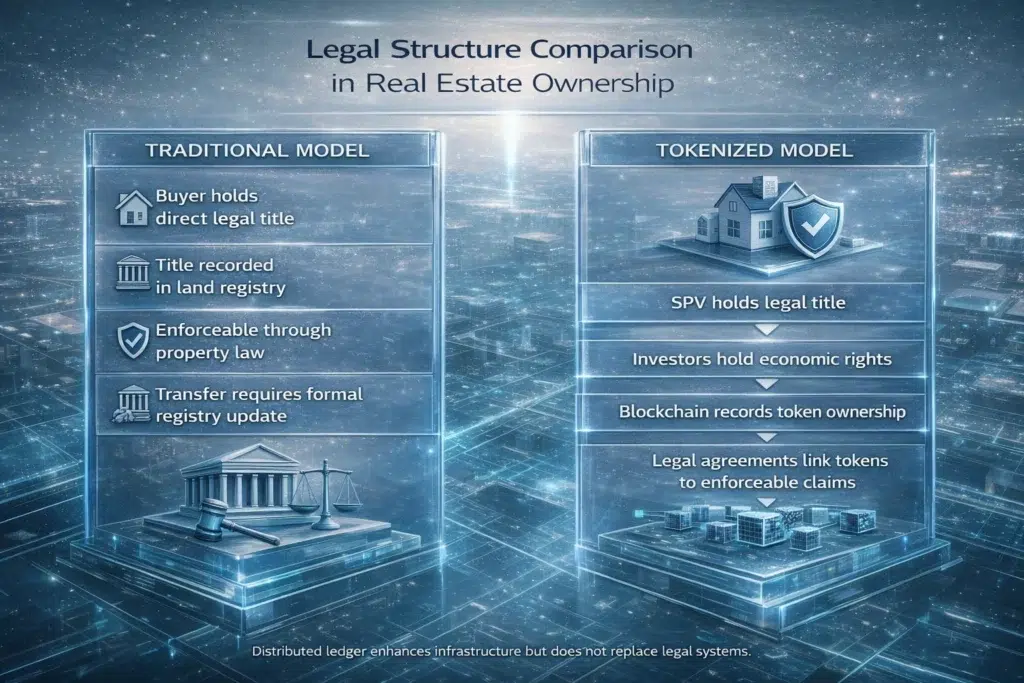

Traditional Model: Direct Legal Title

In traditional property investment, the buyer holds direct legal title. That title is recorded in a government land registry (the official government database of property ownership). Ownership is directly enforceable in court. Transfer requires formal documentation and a registry update. Once the deed is in your name, no third party’s bankruptcy or platform failure can affect your ownership. This is what practitioners mean by Zero Counterparty Risk: the deed is yours independently of any company, platform, or intermediary.

In most jurisdictions, property rights are recorded in government land registries. For certain property investment vehicles such as REITs (Real Estate Investment Trusts, publicly traded funds owning income-producing properties), regulatory oversight falls under frameworks such as the U.S. Securities and Exchange Commission (SEC).

Tokenized Model: Allocated SPV Ownership

In the tokenized model, an SPV holds the legal property title. Investors hold economic rights through digital tokens representing their Allocated interest in the SPV. Blockchain records token ownership. Legal agreements link tokens to enforceable rights in the SPV’s corporate documentation.

This introduces Counterparty Risk (the risk that the SPV, the platform, or the vault fails), which does not exist in direct-title ownership. The SPV structure is designed to mitigate this through Insolvency Remoteness (the legal separation that protects the property from platform debts), but the risk is structural and must be evaluated before engaging with any tokenized structure. For detailed analysis of this legal layer, see Legal Structures Behind Tokenized Real Estate.

Capital Requirements and Accessibility

Capital structure is one of the most practically significant differences when comparing how tokenized real estate works compared to traditional property investment.

Traditional property investment typically requires significant upfront capital, mortgage qualification (if financed), a down payment, closing costs, and legal representation. This concentration of capital in a single asset limits diversification and restricts participation to investors with substantial available funds.

Tokenized real estate may allow fractional participation with smaller capital allocations, enabling diversification across multiple properties. Where platforms operate under compliant regulatory frameworks, entry thresholds can be considerably lower than traditional property purchase requirements. However, securities law compliance may limit participation depending on jurisdiction and investor eligibility rules. Lower minimum investment does not automatically mean unrestricted access.

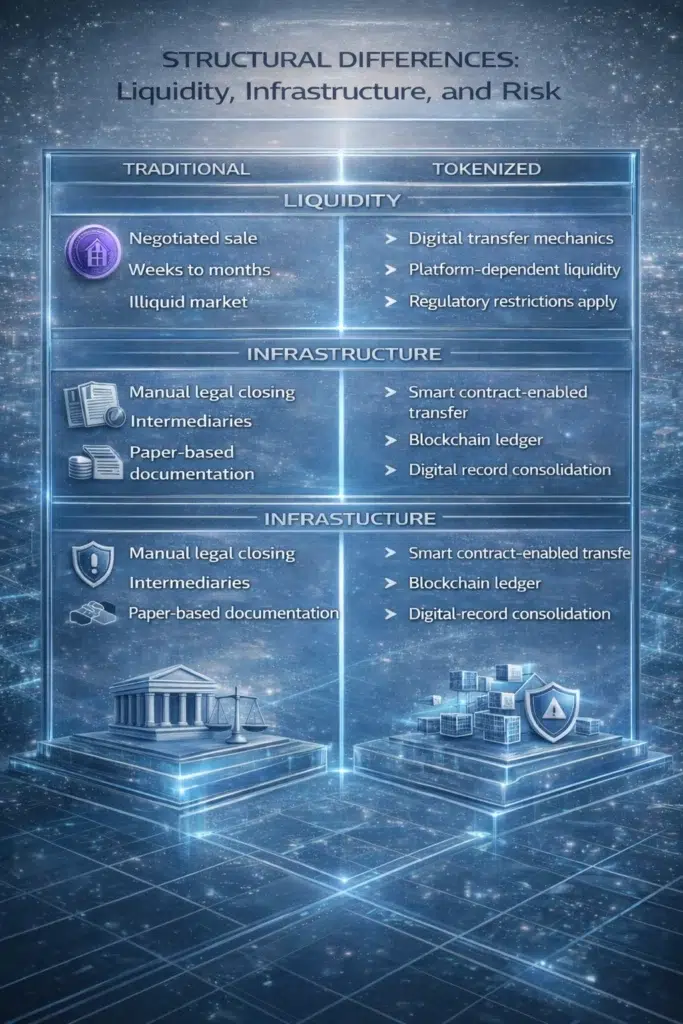

Liquidity and Transfer: The Speed Difference

Liquidity is one of the most discussed dimensions when analyzing how tokenized real estate works compared to traditional property investment, and one of the most important to understand accurately.

Traditional property sales involve listing, negotiation, escrow, notary or legal settlement, and registry updates. Transactions typically take weeks or months. There is also significant Slippage risk (the cost of price movement during a slow transaction, where the agreed price and the final closing price may differ due to time delays). Real estate is traditionally illiquid by design.

Tokenized real estate may allow faster digital transfers using Atomic Settlement (the simultaneous, instant execution of both sides of a token transfer, where buyer receives tokens and seller receives payment in the same transaction with no settlement delay). This can dramatically reduce the time and administrative cost of ownership transfer. However, this speed advantage is conditional on platform infrastructure, regulatory permissions, and secondary market availability.

The critical distinction is between Liquidity and Exit Liquidity (the actual ability to sell a position to a willing buyer with cash). Tokenization provides the infrastructure for faster transfers. It does not guarantee buyers exist at a given moment. Digital transferability does not automatically create deep market liquidity.

Operational Infrastructure Comparison

The operational differences between the two models go beyond ownership structure. The table below compares how each model handles the core administrative functions of property investment.

| Operational Component | Traditional Model | Tokenized Model |

|---|---|---|

| Ownership Registry | Government land registry holds authoritative title record | Blockchain ledger records token ownership alongside legal SPV documentation |

| Settlement Process | Manual legal closing over weeks or months | Smart contract-enabled Atomic Settlement, potentially near-instant |

| Income Distribution | Manual calculation and bank transfer, typically quarterly | Smart contract automation routing NOI proportionally to verified wallets |

| Valuation Transparency | Annual appraisal, slow and manual | Real-Time NAV via on-chain Oracle data feeds (e.g., Chainlink), verifiable continuously |

| Management Model | Active landlord responsibilities or manually hired property manager | Professional PropTech (property technology) management, passive for token holders |

| Counterparty Risk | Zero Counterparty Risk once deed is held directly | Counterparty Risk present via SPV, platform, and custody layer |

| Ownership Units | Whole property or direct fractional title | Allocated fractional digital tokens in an SPV |

Applied Example: A $5,000,000 Commercial Property

A concrete example clarifies how tokenized real estate works compared to traditional property investment in practice. Consider a commercial office building valued at $5,000,000.

Traditional Scenario

An investor purchases the property outright. Legal title is recorded in the government registry in the investor’s name. Rental income is received directly into the investor’s bank account. Managing the property requires either active landlord involvement or hiring and monitoring a property manager. A sale requires the full legal transfer process: listing, negotiation, escrow, notary or legal settlement, and registry update. The investor has Zero Counterparty Risk but high capital concentration and limited liquidity.

Tokenized Scenario

The property is transferred to an Insolvency-Remote SPV. 50,000 tokens are issued at $100 each, representing 100% of the SPV ownership. An investor purchasing 500 tokens holds a 1% Allocated interest in the SPV. Rental income, specifically the NOI (Net Operating Income, total rent minus all operating expenses), is collected by a professional PropTech management firm and distributed proportionally via smart contract to all verified token holders, potentially as On-Chain Yield (digital income payments in stablecoins, which are blockchain-based currencies designed to maintain a stable value relative to a reference currency such as the US dollar). Real-Time NAV updates via Oracle data feeds allow the investor to see the current value of their 500 tokens at any time. Transfer of tokens on a compliant secondary market may occur far faster than a traditional property sale, subject to platform and regulatory conditions.

In both scenarios, enforceability derives from property and corporate law. The token structure does not replace legal enforceability. It changes how that enforceability is accessed and administered.

Risk Framework: Where Each Model Creates Exposure

A balanced understanding of how tokenized real estate works compared to traditional property investment requires evaluating where risk is concentrated in each model. The risk profiles are structurally different, not simply better or worse.

Traditional Property Risks

- Illiquidity: difficulty selling at fair value quickly, especially in weak markets

- Capital concentration: large single-asset exposure with limited diversification

- Tenant default: loss of rental income if tenants fail to pay

- Market downturn: property value decline in adverse economic conditions

- Maintenance costs and active management obligations

Tokenized Real Estate Risks

- Counterparty Risk: SPV, platform, or custody layer failure affecting access to ownership

- Regulatory classification risk: securities law uncertainty in evolving frameworks

- Platform dependency: digital access disruption if the platform ceases to operate

- Smart contract vulnerability: coding errors that can affect income distribution or transfers

- Legal-digital synchronization risk: gaps between what the blockchain records and what the physical property situation actually is (the Oracle Problem)

- Exit Liquidity risk: no guarantee of buyers at a given moment despite transfer infrastructure

The European Securities and Markets Authority (ESMA) has examined distributed ledger integration and emphasized the importance of governance safeguards in managing these risks. No infrastructure eliminates legal or market risk entirely. For a detailed breakdown of tokenized real estate risks, see Benefits and Risks of Tokenized Real Estate and Benefits and Risks of RWA Tokenization.

Regulatory and Compliance Considerations

Both traditional and tokenized real estate operate within enforceable legal frameworks. The regulatory layers differ significantly, however. Traditional property investment is governed primarily by property law and contract law, with securities law applying only to certain pooled vehicles such as REITs.

Tokenized real estate may intersect with securities law (if tokens are classified as investment contracts), property law (governing the underlying asset), corporate law (governing the SPV), custody regulation (governing how tokens and titles are held), and AML (Anti-Money Laundering) frameworks requiring identity verification of all participants. Regulatory oversight may involve the SEC, the European Securities and Markets Authority (ESMA), national regulators, or jurisdiction-specific frameworks such as VARA (Virtual Assets Regulatory Authority) in Dubai or MiCA (Markets in Crypto-Assets Regulation) in the EU.

Regulatory alignment is essential when evaluating how tokenized real estate works compared to traditional property investment. For regulatory context, see What Is VARA Regulation and What Is MiCA Regulation.

Key Structural Differences Summary

Traditional property relies on direct legal title ownership with Zero Counterparty Risk once the deed is held. Tokenized real estate relies on Allocated digital representation through an SPV, introducing Counterparty Risk but enabling fractional access and programmable administration. Traditional transfers involve manual legal processes with significant Slippage potential. Tokenized transfers use Atomic Settlement via blockchain infrastructure with compliance checks built into the transfer mechanism. Traditional liquidity is slow, negotiated, and capital-intensive to exit. Tokenized liquidity depends on compliant digital platforms and actual Exit Liquidity in the market. Both rely on enforceable legal systems. Neither eliminates property-level market risk.

The Hybrid Portfolio Perspective

Sophisticated investors increasingly treat these models as complementary rather than competing. Traditional direct-title ownership serves as foundational wealth: the core assets where Zero Counterparty Risk matters most and where long-term capital preservation is the priority. Tokenized fractional ownership serves active portfolio rebalancing: providing efficient exposure to diversified, higher-yield niches such as data centers, logistics facilities, or medical offices without requiring full property-scale capital commitments.

Understanding the Insolvency-Remote SPV structure, the Allocated nature of token ownership, and the difference between infrastructure liquidity and Exit Liquidity is the foundation of any informed comparison between these two models.

FAQ: How Tokenized Real Estate Works Compared to Traditional Property Investment

Is tokenized real estate safer than traditional property?

Safety depends on what dimension you are evaluating. Traditional direct-title offers Zero Counterparty Risk: your deed cannot be affected by platform bankruptcy. Tokenized real estate introduces Counterparty Risk via the SPV, platform, and custody layer, but may reduce concentration risk through fractional diversification. Neither model is universally safer. The risk profiles are structurally different.

How does liquidity differ between the two models?

Traditional property liquidity depends on negotiated sales that can take months and carry Slippage risk. Tokenized real estate may allow faster transfers via Atomic Settlement infrastructure. However, true Exit Liquidity (a willing buyer with cash) is not guaranteed by the infrastructure alone. Both models can be illiquid in weak markets with limited buyer demand.

Can tokenized property replace traditional ownership?

No. Tokenization operates alongside legal property systems. It does not replace direct legal title, land registries, or property law. The two models serve different purposes and carry different risk profiles. Many sophisticated investors use both in complementary ways.

Is tokenized real estate legally recognized?

Legal recognition depends on jurisdiction and asset structure. In jurisdictions with clear digital asset frameworks such as the UAE under VARA or the EU under MiCA, legally structured tokenized real estate can have defined regulatory standing. In jurisdictions without specific frameworks, enforceability depends on alignment with existing property and securities law.

What is the difference between Allocated and Unallocated ownership in tokenized real estate?

Allocated ownership means your token is linked to a specific, identifiable interest in a specific property through a specific SPV. Unallocated ownership means you hold a general claim against a pool with no specific asset backing. All institutional-grade tokenized real estate structures are Allocated. Unallocated structures carry significantly weaker legal protection and should be evaluated with extreme caution.

Conclusion

Understanding how tokenized real estate works compared to traditional property investment requires evaluating legal structure, liquidity mechanics, risk exposure, and regulatory alignment together, not in isolation.

Traditional property investment offers Zero Counterparty Risk through direct legal title recorded in government registries. It requires significant capital, carries active management obligations, and is structurally illiquid. Tokenized real estate introduces Allocated fractional ownership through Insolvency-Remote SPVs, enabling lower entry thresholds, programmable income distribution via smart contracts, Real-Time NAV transparency through on-chain Oracle data feeds, and potential Atomic Settlement on compliant secondary markets. It introduces Counterparty Risk that traditional ownership does not have.

Tokenization modernizes ownership infrastructure. It does not replace property law. Both models rely on enforceable legal systems, regulatory compliance, and underlying property market fundamentals. The choice between them, or the decision to use both in a hybrid portfolio, depends on the specific objectives, risk tolerance, and capital profile of each investor.

Sources and Regulatory References

- Bank for International Settlements (BIS): https://www.bis.org

- U.S. Securities and Exchange Commission (SEC): https://www.sec.gov

- European Securities and Markets Authority (ESMA): https://www.esma.europa.eu

Educational Disclaimer

This article is provided for educational purposes only and does not constitute financial, legal, or investment advice. Regulatory treatment of tokenized real estate varies by jurisdiction and asset classification. Professional legal consultation should be obtained before engaging with any tokenized property structure.

Last updated: March 2026

Explore Tokenized Real Estate

- Tokenized Real Estate Explained

- Fractional Ownership in Tokenized Real Estate

- Legal Structures Behind Tokenized Real Estate

- Benefits and Risks of Tokenized Real Estate

- What Types of Properties Can Be Tokenized

- Benefits and Risks of RWA Tokenization (cluster)

- Real-World Asset Tokenization Explained (cluster)

- Why Compliance Matters in Tokenized Finance (cross-pillar)

- On-Chain Transparency Explained (cross-pillar)

- Real-World Assets Hub

{kind=link}