Fractional Ownership in Tokenized Real Estate: Structure, Rights, Governance, and Risks Explained

This article is part of the broader Real-World Assets educational framework, explaining how fractional ownership in tokenized real estate works in practice, what rights token holders receive, how governance is structured, and what risks must be evaluated before engaging with any tokenized property structure.

Educational Notice

This article is provided for informational and educational purposes only. It does not constitute financial, legal, or investment advice. Regulatory treatment of fractional ownership in tokenized real estate varies by jurisdiction and asset classification. This guide does not promote any investment strategy.

Introduction

Fractional ownership in tokenized real estate combines traditional shared property ownership structures with blockchain-based digital infrastructure. The concept is not as new as it might appear. Real estate has long been owned by multiple investors through syndications, partnerships, tenancy structures, and corporate entities. What tokenization adds is a digital record-keeping layer that allows ownership units to be tracked, verified, and transferred more efficiently, while preserving enforceable legal rights.

Imagine trying to buy one-thousandth of an apartment building using old legal methods. The paperwork, valuation fees, and legal costs would exceed the investment itself. Traditional fractional ownership through syndications has always been slow, expensive, and largely reserved for wealthy insiders. Tokenization addresses this by creating what practitioners describe as Frictionless Syndication: the same legal structure, but delivered through programmable digital infrastructure that reduces friction at every step.

In fractional ownership in tokenized real estate, a property is legally structured, often through an SPV (Special Purpose Vehicle, a separate legal entity created to hold a single asset), and ownership units are divided into defined shares. Digital tokens represent those shares. These tokens do not replace legal ownership. They reflect legally enforceable economic rights tied to the property through that legal entity.

If you are new to tokenized real estate more broadly, these articles provide useful context:

- Tokenized Real Estate Explained

- How Tokenized Real Estate Works Compared to Traditional Property Investment

- Legal Structures Behind Tokenized Real Estate

- Benefits and Risks of Tokenized Real Estate

The Bank for International Settlements (BIS) has emphasized that distributed ledger technologies (shared databases maintained simultaneously across multiple participants) enhance existing financial infrastructure but do not replace legal systems. That principle applies directly here: tokenization improves how fractional ownership is administered. It does not change the legal foundations that make ownership enforceable.

In Simple Terms: What Is Fractional Ownership in Tokenized Real Estate?

Fractional ownership in tokenized real estate means dividing a property into smaller ownership units that are represented by digital tokens. Each token holder owns a proportional economic share of the underlying asset through a legally structured entity, while blockchain records that ownership digitally.

A critical distinction that professional investors always verify: is the ownership Allocated or Unallocated? Allocated ownership means you hold a specific, identifiable interest in a specific property through a defined legal entity such as an SPV. Unallocated ownership means you are a general creditor of a pool with no specific asset backing your claim. Institutional-grade tokenized real estate structures are always Allocated. Unallocated structures offer far weaker legal protection and should be evaluated with significant caution.

What Is Fractional Ownership in Tokenized Real Estate?

Fractional ownership in tokenized real estate refers to dividing a property into multiple legally defined ownership units that are digitally represented through blockchain-based tokens. The typical structure follows a clear sequence: a property is legally owned by an entity (usually an SPV), ownership interests in that entity are divided into defined units, digital tokens correspond to those units, investors acquire tokens representing proportional economic rights, and income and governance rights are allocated based on token holdings.

This structure enables shared participation in real estate assets while maintaining enforceable legal rights. The property stays in the SPV. The SPV stays in the legal system. The tokens reflect what you hold in the SPV. Each layer has its own governing rules.

Fractional Ownership Before Tokenization

Before blockchain technology, fractional ownership already existed in real estate markets through several well-established models. Understanding these predecessors is important because tokenization builds on them rather than replacing them.

Tenancy in Common (TIC)

Multiple individuals hold direct title to a property, each owning a defined percentage. Each owner’s share may be transferred independently, subject to agreement terms. TIC structures are legally straightforward but administratively cumbersome at scale, particularly when managing income distributions across many co-owners.

Real Estate Syndications

Investors pool capital through a limited partnership or corporation that acquires property. Investors hold units in the entity rather than direct title. Syndications have been used by institutional investors for decades but typically require high minimum investments and manual administrative processes.

Real Estate Investment Trusts (REITs)

REITs (Real Estate Investment Trusts, publicly traded funds that pool investor capital to own income-producing properties) allow investors to purchase shares representing interests in portfolios of income-producing properties. In the United States, REITs operate under securities law frameworks. They provide liquidity through stock exchange trading but do not allow investors to hold interests in specific properties.

Fractional ownership is therefore a legal and financial structure embedded in corporate and property law. Tokenization digitizes this structure, reduces its administrative overhead, and potentially makes it accessible to a wider range of investors. The legal concept is established. The delivery mechanism is new.

The 4 Steps to Digital Fractionalization

Think of the tokenization process as a digital factory where a building enters on one end and tokens exit on the other. Each step serves a specific legal and operational function.

Step 1: The Vaulting (SPV Lockup)

A reputable manager selects an income-producing property, typically one with documented rental income and clear legal title. That property is legally transferred into a separate company called an SPV. The SPV holds the real-world deed. This structure is designed to be Insolvency Remote (legally protected from platform debts), meaning if the tokenization platform goes bankrupt, the building is ring-fenced and safe from their creditors. The first question every serious investor should ask is: Is this SPV isolated from platform debts, and is that isolation documented in the legal agreements?

Step 2: The Unitization (Cutting the Pie)

Ownership of that SPV is then divided into precise, uniform digital units called tokens. Authoritative platforms use specific security token standards such as ERC-1400 or ERC-3643 (technical standards for security tokens on blockchain networks that have Transfer Restrictions built directly into the code). These standards ensure that only legally verified, KYC-compliant investors can hold or receive the tokens. Non-compliant wallets are automatically blocked from receiving transfers, making regulatory compliance programmable rather than manual.

Step 3: The Rights Allocation (Coding the Income)

Once the property is tokenized, the smart contract automatically assigns rights to every token holder based on their proportional holdings. If you own 1% of the tokens, the smart contract routes 1% of the rental profit, specifically the NOI (Net Operating Income, meaning total rental income minus all operating expenses), directly to your verified digital wallet. The same logic applies to governance: if you own 1% of the tokens, you hold 1% of the vote on major decisions. No paper checks. No manual accounting. The distribution rules are enforced by code.

Identity Oracles (automated verification systems connected to the smart contract that check KYC and AML status before permitting a wallet to hold tokens) handle compliance automatically. Only Whitelisted wallets (wallets that have passed identity verification and been approved to hold the token) can receive distributions or participate in governance votes. This makes the compliance layer continuous rather than one-time.

Step 4: The Real-Time Verification (NAV)

How does a token holder know what their share is worth at any given moment? Leading platforms use on-chain valuations and Real-Time NAV (Net Asset Value, the current market value of the underlying property divided by the total number of tokens outstanding). An independent appraiser updates the building’s value at defined intervals. An Oracle (a data feed mechanism that connects real-world information to a blockchain) feeds that data to the smart contract. The token’s NAV is updated based on verified external data rather than platform claims. For further context on verification mechanisms, see What Is Proof of Reserve and On-Chain Transparency Explained.

Legal Structure Behind Fractional Ownership

The SPV is the legal anchor of the entire structure. The SPV legally owns the property. The SPV issues ownership units. Digital tokens represent those units. Investors hold economic rights linked to the SPV. Corporate law governs the SPV. Property law governs the asset. Blockchain records token ownership. The legal entity, not the blockchain, confers enforceable rights.

Governance in Fractional Ownership

Fractional ownership in tokenized real estate requires clearly defined governance rules covering decision-making authority, voting rights where applicable, distribution policies, asset sale procedures, and exit mechanisms. Governance provisions must be codified in operating agreements, not merely implied by the token structure.

One significant governance risk that is often under-discussed is Whale Risk: the possibility that a single large token holder (a “Whale”) accumulates enough tokens to outvote all smaller fractional investors combined. In a standard one-token-one-vote system, a holder with 51% of tokens controls all decisions. Some platforms address this through Quadratic Voting (a governance mechanism where voting power increases less than proportionally with token holdings, giving smaller holders more relative influence), which reduces the risk of majority control by a single large participant. Governance documentation should be reviewed carefully to understand exactly how voting power is structured.

Depending on jurisdiction and structure, tokenized fractional ownership may be treated as a security. Regulatory oversight may involve the U.S. Securities and Exchange Commission (SEC) or the European Securities and Markets Authority (ESMA). Compliance determines enforceability. For regulatory context, see Why Compliance Matters in Tokenized Finance.

Ownership Rights in Fractional Tokenized Real Estate

Fractional ownership in tokenized real estate generally confers four categories of proportional rights, each arising from legal agreements rather than from blockchain technology itself.

Economic Rights

- Proportional share of rental income distributions based on verified NOI

- Proportional share of proceeds upon property sale

- Participation in appreciation where structured into the token agreement

Governance Rights

- Voting on major decisions such as property sale or refinancing, where defined

- Participation in structural amendments to the SPV agreement

- Approval of asset disposition where governance rules permit

Transfer Rights

- Transfer of tokens to other verified, Whitelisted wallets subject to regulatory restrictions

- Secondary trading where platform infrastructure and regulatory permissions allow

Information Rights

- Access to financial reporting and property performance data

- Ownership transparency through on-chain records

- Access to Real-Time NAV updates verified through Oracle data feeds

Income Distribution: Traditional vs Tokenized

One of the clearest practical differences between traditional and tokenized fractional ownership is how income is distributed to investors. The comparison below illustrates the operational shift.

| Component | Traditional Fractional (Syndication) | Tokenized Fractional |

|---|---|---|

| Minimum Investment | Typically $25,000 or more | Potentially $50 or more depending on platform |

| Yield Distribution | Quarterly or annual via manual calculation and bank transfer | Monthly or more frequent via smart contract automation |

| Valuation Transparency | Manual audits, periodic reporting, limited visibility | Real-Time NAV updated via Oracle data feeds, verifiable on-chain |

| Compliance Verification | One-time KYC at onboarding, manually managed | Continuous Identity Oracle Whitelisting enforced by smart contract |

| Exit and Transfer | Highly illiquid, often requiring full property sale or lengthy legal process | Potential secondary market trading subject to platform design and regulatory permissions |

| Ownership Proof | Paper-based certificates and corporate registers | Blockchain-based token ownership with Proof of Reserve verification |

Cash movement in both models remains governed by banking systems. Smart contracts automate the calculation and routing logic. The actual transfer of fiat currency still requires traditional banking infrastructure in most structures.

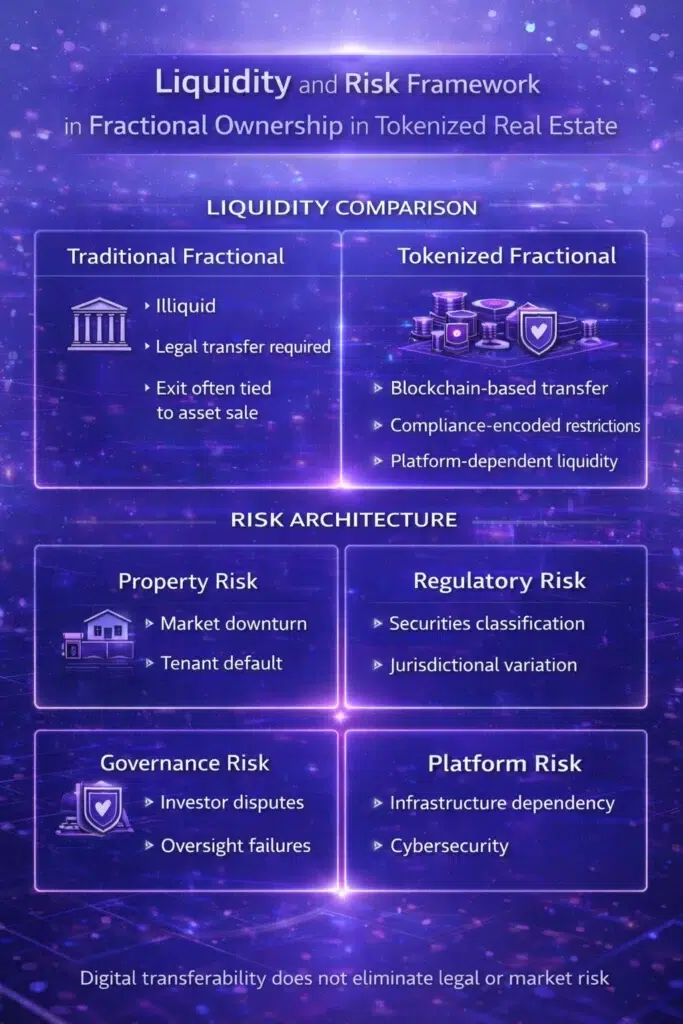

Liquidity and Transferability

Liquidity is one of the most discussed aspects of fractional ownership in tokenized real estate, and one of the most frequently misunderstood. Traditional fractional ownership is often illiquid: transfers require legal documentation, secondary markets are limited, and exit may require a full property sale agreed upon by all co-owners. Tokenized fractional ownership offers the infrastructure for blockchain-based transfers with encoded compliance rules. But platform-dependent liquidity and regulatory constraints still apply.

The OECD (Organisation for Economic Co-operation and Development) has examined distributed ledger technologies as tools for enhancing transparency and record integrity. But even with improved infrastructure, Exit Liquidity (the actual ability to sell a position to a willing buyer with cash) remains dependent on real market demand. Liquidity potential does not eliminate market risk or guarantee a buyer at any given moment.

Risks of Fractional Ownership in Tokenized Real Estate

Balanced evaluation is essential. The efficiency improvements of tokenization are real, but they exist alongside a distinct set of risks that must be understood before engaging with any fractional structure.

Underlying Property Risk

Market downturns, tenant default, vacancy periods, and maintenance costs all remain regardless of how ownership is recorded. Tokenization does not change the fundamentals of the underlying property market.

Regulatory Risk

Securities classification uncertainty, jurisdictional variation across different countries, and cross-border compliance complexity can all affect the validity and enforceability of tokenized fractional structures. Regulatory frameworks continue to evolve. For an overview, see What Is MiCA Regulation and What Is VARA Regulation.

Governance Risk

Disputes among token holders, ambiguous voting rights, and Whale Risk (where a single large holder controls outcomes for all smaller investors) can undermine governance quality. Platforms using Quadratic Voting (a system that reduces the proportional voting power of very large holders to protect smaller participants) mitigate this risk, but governance design must be reviewed in the legal agreements, not assumed.

Platform Risk

Infrastructure dependency and cybersecurity vulnerabilities mean that platform failure can disrupt access to digital ownership records even when the underlying legal ownership remains intact. The SPV protects the asset. It does not protect digital access if the platform ceases to operate.

Smart Contract Risk

Coding errors and execution bugs can affect income distribution, transfer restrictions, and compliance enforcement. Independent Smart Contract Audits by specialist firms are the institutional standard for managing this risk before a platform launches any tokenized structure.

Regulatory and Compliance Considerations

Fractional ownership in tokenized real estate may fall under securities law depending on how the structure is designed and how tokens are offered to investors. Key compliance considerations include investor eligibility rules (determining who can legally hold the tokens), AML (Anti-Money Laundering) and KYC (Know Your Customer) requirements, disclosure standards governing what information must be shared with investors, custody obligations for both the physical property title and the digital tokens, and ongoing reporting duties to regulatory authorities.

In practice, Identity Oracle Whitelisting handles much of the ongoing compliance enforcement automatically. But the underlying legal framework, the securities classification decision, and the disclosure documentation are all human-driven legal processes that must be completed correctly before any tokens are issued. Legal enforceability remains jurisdiction-dependent. Regulatory classification must be determined before token issuance, not after.

For broader compliance context, see Why Compliance Matters in Tokenized Finance and Benefits and Risks of RWA Tokenization.

FAQ: Fractional Ownership in Tokenized Real Estate

Is fractional ownership in tokenized real estate the same as tokenization?

No. Fractional ownership divides property ownership into defined units through a legal structure such as an SPV. Tokenization represents those units digitally on a blockchain. The two concepts work together: fractional ownership is the legal layer, tokenization is the digital record-keeping layer. Neither works properly without the other.

Do fractional token holders own the property directly?

Typically, no. The SPV owns the property. Token holders own economic rights in the SPV, specifically Allocated rights to income distributions and sale proceeds. This is legally distinct from direct property ownership. Courts enforce rights based on the SPV’s corporate documents, not on blockchain records.

What is the difference between Allocated and Unallocated ownership?

Allocated ownership means your token is linked to a specific, identifiable interest in a specific property held by a specific SPV. Unallocated ownership means you hold a general claim against a pool with no specific asset backing your position. Institutional-grade tokenized real estate is always Allocated. Unallocated structures carry significantly weaker legal protection.

Is fractional ownership in tokenized real estate legally recognized?

Recognition depends on jurisdiction and regulatory classification. In jurisdictions with clear digital asset frameworks such as the UAE under VARA (Virtual Assets Regulatory Authority) or the EU under MiCA (Markets in Crypto-Assets Regulation), legally structured tokenized fractional ownership can have clear regulatory standing. In jurisdictions without specific frameworks, enforceability depends on how closely the structure aligns with existing property and securities law.

Can fractional tokens be resold?

Transferability depends on regulatory rules and platform structure. Tokens using standards such as ERC-1400 or ERC-3643 have Transfer Restrictions built into the code: only Whitelisted wallets that have passed KYC and AML verification can receive tokens. Secondary trading is possible where permitted by regulation and where the platform provides the necessary infrastructure, but Exit Liquidity (finding a willing buyer with cash) is never guaranteed.

What is Whale Risk in tokenized governance?

Whale Risk refers to the possibility that a single large token holder accumulates enough tokens to control all voting outcomes in a one-token-one-vote system. If a single entity holds more than 50% of tokens, they can override all smaller investors on major decisions such as property sale or governance changes. Platforms using Quadratic Voting (a system giving smaller holders more relative voting influence) reduce this risk, but it must be verified in the governance documentation.

Conclusion

Fractional ownership in tokenized real estate represents the modernization of real estate syndication, not its replacement. The legal concepts are established. The delivery mechanism is new. By using Allocated SPV structures, Identity Oracle Whitelisting, Real-Time NAV verification, and security token standards such as ERC-1400 or ERC-3643, tokenization provides a faster, more transparent, and potentially more accessible form of fractional ownership built for institutional stability.

But the legal framework remains primary. Property law governs the underlying asset. Securities law governs how interests are offered and sold. Governance documentation governs what token holders can actually do. And regulatory compliance determines whether the entire structure holds up when tested. Fractional ownership in tokenized real estate modernizes operational efficiency while preserving the legal foundation that makes ownership enforceable.

Sources and Regulatory References

- Bank for International Settlements (BIS): https://www.bis.org

- Organisation for Economic Co-operation and Development (OECD): https://www.oecd.org

- U.S. Securities and Exchange Commission (SEC): https://www.sec.gov

- European Securities and Markets Authority (ESMA): https://www.esma.europa.eu

Educational Disclaimer

This article is provided for educational purposes only and does not constitute financial, legal, or investment advice. Regulatory treatment of fractional ownership in tokenized real estate varies by jurisdiction and asset classification. Professional legal consultation should be obtained before engaging with any tokenized property structure.

Last updated: March 2026

Explore Tokenized Real Estate

- Tokenized Real Estate Explained

- How Tokenized Real Estate Works Compared to Traditional Property Investment

- Legal Structures Behind Tokenized Real Estate

- Benefits and Risks of Tokenized Real Estate

- What Types of Properties Can Be Tokenized

- Benefits and Risks of RWA Tokenization (cluster)

- Why Compliance Matters in Tokenized Finance (cross-pillar)

- What Is Proof of Reserve (cross-pillar)

- On-Chain Transparency Explained (cross-pillar)

- Real-World Assets Hub

{kind=link}