Benefits and Risks of Tokenized Real Estate: Structure, Opportunities, and Regulatory Considerations Explained

This article is part of the broader Real-World Assets educational framework, providing a balanced analysis of the key benefits and risks of tokenized real estate across legal enforceability, regulatory classification, governance design, technology integrity, liquidity structure, and underlying property market exposure.

Educational Notice

This article is provided for informational and educational purposes only. It does not constitute financial, legal, or investment advice. Regulatory treatment of tokenized real estate varies by jurisdiction and asset classification. This guide does not promote any investment strategy.

Introduction: The Coat Check Ticket

Tokenizing a real-world asset is a lot like a professional coat check. You hand your heavy, physical coat (the property title) to an attendant (the platform). They give you a lightweight, numbered ticket (the token). That ticket is easy to carry, easy to trade, and instantly proves you are the rightful owner. You can sell it to anyone in the theater at any time.

But here is the thing: the risk is never really in the ticket itself. The risk is in the coat check stand, which in real estate tokenization means the SPV (Special Purpose Vehicle, a separate legal entity created to hold the asset), the vault, the platform, and the regulatory environment surrounding all of it. If the stand burns down, if the attendant is dishonest, or if the rules of the theater change overnight, that digital ticket can become worthless regardless of how well it was designed.

This article provides a balanced, expert analysis of the benefits and risks that define tokenized real estate. Both sides matter equally. Neither can be understood without the other.

If you are new to this asset class, these articles provide useful context:

- Tokenized Real Estate Explained

- How Tokenized Real Estate Works Compared to Traditional Property Investment

- Fractional Ownership in Tokenized Real Estate

- Legal Structures Behind Tokenized Real Estate

In Simple Terms: What Are the Benefits and Risks of Tokenized Real Estate?

The benefits of tokenized real estate include fractional ownership access, digital transfer infrastructure, improved transparency, and operational efficiency. The risks include regulatory uncertainty, platform dependency, smart contract vulnerabilities, the Oracle Problem (the gap between what a blockchain knows and what is happening in the physical world), liquidity limitations, and traditional property market exposure.

Both dimensions exist simultaneously. A useful starting point: tokenization does not make a bad property good, and it does not make a risky market safe. What it does is change how ownership is recorded, transferred, and governed. Whether that produces better outcomes depends entirely on the quality of the legal structure, the governance design, and the regulatory compliance surrounding the asset.

Why Tokenized Real Estate Is Emerging

Traditional real estate markets have long been characterized by high capital requirements that exclude smaller participants, slow and manual documentation processes, structural illiquidity (the difficulty of selling quickly at fair value), and fragmented record systems spread across registries, banks, and legal offices. These are genuine inefficiencies that have persisted because the alternatives have historically been equally cumbersome.

Digital financial infrastructure has encouraged experimentation with blockchain-based ownership systems as a potential improvement. The Bank for International Settlements (BIS) has noted that distributed ledger technologies (shared databases maintained simultaneously across multiple participants) may enhance settlement efficiency and record integrity in financial systems. The OECD (Organisation for Economic Co-operation and Development) has similarly examined blockchain as a modernization tool for financial market infrastructure.

Tokenized real estate emerges at the intersection of property law and digital infrastructure modernization. It does not replace either. It attempts to make them work together more efficiently.

The 4 Key Benefits: Frictionless Ownership

1. Fractional Accessibility

Traditional real estate requires significant capital. A multi-million dollar apartment building is simply out of reach for most individual participants. Tokenization allows that same building to be fractionalized (divided into thousands of smaller digital ownership units), potentially enabling participation at much lower thresholds and allowing diversification across multiple properties rather than concentration in a single asset.

It is important to note that fractionalization itself is not new. REITs (Real Estate Investment Trusts, publicly traded funds that pool investor capital to own income-producing properties) and traditional real estate syndications have long enabled shared ownership. What tokenization adds is digital infrastructure: programmable transfer rules, automated compliance checks, and reduced intermediary costs. The concept is established. The delivery mechanism is new. Securities law compliance may still limit participation depending on jurisdiction and investor eligibility rules.

2. Operational Efficiency

Traditional property transactions involve title searches, escrow processes (third-party holding of funds during a transaction), manual documentation, and registry updates that can take weeks. Tokenized systems may streamline certain elements by digitally recording ownership units, automating transfer logic through smart contracts, and reducing reconciliation needs across fragmented systems. Blockchain-based synchronization can reduce the Information Asymmetry (gaps in data between different parties in a transaction) and coordination errors common in manual property administration.

One important caveat: operational efficiency on the technology layer does not override legal documentation requirements. The SPV still needs its corporate documents. The land registry still needs its title record. Technology speeds up coordination. It does not eliminate legal process.

3. Transparency and Auditability

Blockchain ledgers create timestamped ownership records that are visible and verifiable. Every token transfer, every income distribution, and every on-chain governance vote is recorded on an immutable ledger (a permanent, tamper-resistant database). This provides a level of real-time auditability that traditional corporate records cannot easily replicate.

However, on-chain transparency of token transfers does not replace corporate agreements, SPV documentation, or property registry records. A blockchain entry showing that a wallet holds tokens is not the same as a corporate register showing equity in an SPV. Courts remain authoritative over property and ownership disputes. The transparency layer is useful for record-keeping and governance monitoring. It is not a substitute for legal enforceability.

4. Potential Liquidity Enhancement

Traditional real estate is typically illiquid. Selling a property or a conventional share in one can take months. Tokenization provides the infrastructure for a 24/7 global secondary market where tokens could potentially be transferred faster than traditional settlement allows, with programmable compliance checks verifying buyer eligibility automatically.

But a critical distinction must be understood here: liquidity potential is not the same as Exit Liquidity (the actual ability to sell your position to a real buyer with cash). If there are no buyers on the platform, the token is just as illiquid as the physical property it represents. The infrastructure exists. The market depth may not. Liquidity potential must never be confused with liquidity certainty.

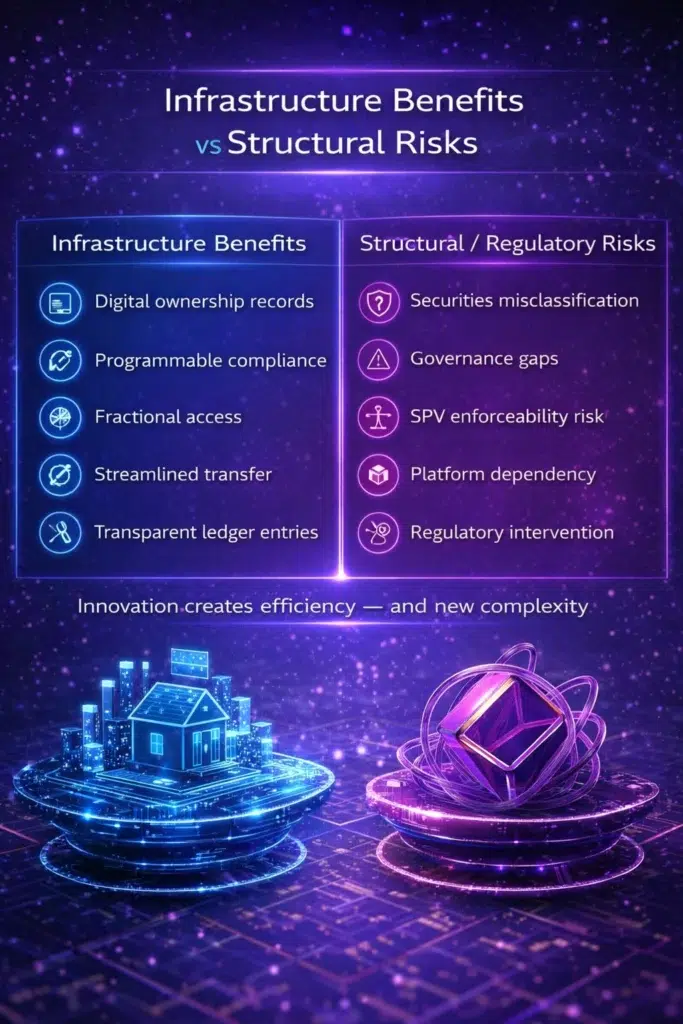

Infrastructure Benefits vs Structural Risks: A Direct Comparison

The benefits and risks of tokenized real estate often arise from exactly the same structural innovations. The table below maps each benefit directly to the corresponding risk it introduces, because understanding this relationship is essential to evaluating any tokenized real estate structure honestly.

| Infrastructure Benefit | Corresponding Structural Risk |

|---|---|

| Digital ownership records improve traceability | Securities misclassification risk if tokens are improperly structured |

| Programmable compliance via smart contracts | Smart contract vulnerabilities and coding execution errors |

| Fractional access lowers participation thresholds | SPV enforceability risk if Insolvency Remoteness is not properly structured |

| Streamlined digital transfers reduce friction | Platform dependency risk if the technology provider fails or shuts down |

| Transparent ledger entries improve auditability | Oracle Problem: blockchain cannot see physical world changes without human input |

| 24/7 secondary market infrastructure | Exit Liquidity risk: infrastructure exists but market depth may not |

The Core Risks: The Coat Check Stand Vulnerabilities

Understanding the risks of tokenized real estate requires a clear hierarchy. Not all risks are equal. Some failures are recoverable. Others are not. The framework below organizes risks from most foundational to most operational, because if the foundation is broken, nothing above it can be fixed.

Layer 1 – The Foundation: Legal and Regulatory Risk

Regulatory uncertainty is the most foundational risk in tokenized real estate. If this layer is broken, nothing else matters. Depending on how a structure is designed, tokenized interests may be classified as securities by regulators such as the U.S. Securities and Exchange Commission (SEC) or the European Securities and Markets Authority (ESMA), triggering registration requirements, disclosure obligations, investor eligibility restrictions, and ongoing reporting duties.

Related to this is Insolvency Remoteness (also called Bankruptcy Remoteness), the legal protection that keeps an SPV’s property legally separated from the debts of the platform operating around it. If Insolvency Remoteness is not properly structured, a platform bankruptcy could allow creditors to make claims against the property held in the SPV. Token holders would then be competing with creditors for assets they believed were fully protected. This is the single most important legal concept in tokenized real estate. For detailed context, see Legal Structures Behind Tokenized Real Estate and Why Compliance Matters in Tokenized Finance.

Layer 2 – The Core: Smart Contract Vulnerabilities and Custody Risk

The rules governing token ownership, income distribution, and transfer restrictions are written in computer code called smart contracts. Smart contract vulnerabilities (bugs or flaws in the code that can be exploited) represent a significant technical risk. In traditional finance, a processing error might delay a payment. In tokenization, an unpatched vulnerability could allow a malicious actor to drain an SPV treasury or rewrite ownership records entirely. This is what industry practitioners call the Digital Heist risk.

Institutions managing this risk require independent Smart Contract Audits conducted by reputable specialist firms before deployment. Firms such as OpenZeppelin and CertiK perform these audits, reviewing code line by line for vulnerabilities and issuing public reports. An unaudited smart contract in a tokenized real estate structure is a significant red flag regardless of how credible the platform appears otherwise.

Custody risk operates alongside this. Even if legal ownership remains intact, digital access and transfer functionality may be disrupted by platform insolvency, operational shutdown, or cybersecurity breaches. For context on verification and custody frameworks, see What Is Proof of Reserve and On-Chain Transparency Explained.

Layer 3 – The Process: Oracle Problem, Governance, and Liquidity Risk

The Oracle Problem is the single largest point of failure in real-world asset tokenization systems. Blockchains are closed systems. They cannot automatically see or verify what is happening in the physical world. They do not know if a building burned down, if a tenant has vacated, if the local government changed zoning rules, or if a property’s valuation has shifted materially. They rely entirely on Oracles (human inspectors, appraisers, legal officers, or automated data feeds) to supply that physical world information.

If an Oracle provides inaccurate or delayed data, the digital token becomes disconnected from the physical reality it is supposed to represent. The ticket still exists. The coat may no longer be there. This is why institutional-grade tokenization requires independent, verifiable Oracle inputs with audit trails, not just smart contract automation.

Governance risk also operates at this layer. If voting rights are vaguely defined, if token holder rights in the SPV operating agreement are ambiguous, or if there is no clear process for resolving disputes, governance failures can paralyze decision-making at critical moments. Liquidity risk completes this layer: while tokenization provides secondary market infrastructure, Exit Liquidity (the actual ability to sell a position to a willing buyer with cash) depends on market depth that the infrastructure alone cannot guarantee.

Layer 4 – The Result: Underlying Property Market Risk

Tokenization does not eliminate traditional real estate market exposure. Tenant default, vacancy, interest rate sensitivity, property depreciation, and maintenance obligations all remain regardless of how ownership is recorded. Infrastructure modernization does not remove property-level risk. It never has and it never will. A tokenized apartment in a declining market is still an apartment in a declining market.

When Risks May Outweigh Benefits

Risks tend to dominate where SPVs are weakly structured without proper Insolvency Remoteness, where governance documentation leaves investor rights unclear, where regulatory classification has not been formally determined before token issuance, where disclosure standards are inadequate, and where smart contracts have not been independently audited. In these conditions, the infrastructure adds complexity without adding the protections that justify it.

When Benefits May Be Realized

Benefits are more likely to be realized where legal structure is clearly documented with verified Insolvency Remoteness, where securities classification has been formally addressed, where governance mechanisms are transparent and enforceable, where smart contracts have been independently audited with findings addressed, and where reporting is consistent, accessible, and tied to verified Oracle inputs. Infrastructure quality determines outcome. Compliance quality determines sustainability.

For regulatory frameworks that support compliant tokenized structures, see What Is VARA Regulation and What Is MiCA Regulation.

Due Diligence: The Red Flag and Green Flag Checklist

Before evaluating any tokenized real estate structure, the five factors below should each be assessed. A single red flag in the foundation layer is enough to reconsider the entire structure. This checklist reflects institutional-grade evaluation standards.

| Risk Factor | Red Flag | Green Flag |

|---|---|---|

| Legal Structure | No legal wrapper (LLC/SPV) in a recognized jurisdiction | Independent, Insolvency-Remote SPV per property |

| Custody | No independent custodian for title deeds or digital assets | Licensed third-party trust holds titles and digital custody |

| Smart Contract Audit | Unaudited smart contracts with no public audit report | Audited by a reputable firm with all findings addressed |

| Return Claims | Guaranteed yield or fixed return promises | Performance-based distributions tied to verified NOI (Net Operating Income) |

| Regulatory Registration | Registered in an unrecognized or offshore jurisdiction with no regulatory framework | Registered under a recognized framework such as VARA (Dubai), MiCA (EU), or SEC exemptions (US) |

FAQ: Benefits and Risks of Tokenized Real Estate

Is tokenized real estate risky?

Yes. It involves traditional real estate risks such as vacancy, tenant default, and market fluctuations, plus additional regulatory, legal, and technological risks that are specific to the tokenization layer. The two risk categories must be evaluated together, not separately.

Does tokenization remove property market risk?

No. Market conditions, tenant quality, and macroeconomic factors all remain. A tokenized apartment in a weak rental market is still a weak investment. Tokenization changes how ownership is managed. It does not change the underlying economics of the property.

What is the Oracle Problem in tokenized real estate?

The Oracle Problem refers to the gap between what a blockchain records and what is happening in the physical world. A blockchain cannot automatically know if a property burned down, if a tenant left, or if zoning laws changed. It relies on Oracles (human inspectors, appraisers, or data providers) to supply that information. If an Oracle provides inaccurate or delayed data, the digital token becomes disconnected from physical reality.

Why do smart contracts need independent audits?

Smart contract vulnerabilities (bugs in the code governing token rules) can be exploited by malicious actors to drain funds or alter ownership records. Independent audits by specialist firms review code line by line before deployment. An unaudited smart contract in a tokenized real estate structure is a significant risk indicator regardless of platform reputation.

Is liquidity guaranteed in tokenized real estate?

No. Tokenization provides the infrastructure for secondary market trading, but Exit Liquidity (the ability to sell a position to a willing buyer with cash) depends on actual market demand. If there are no buyers on the platform, the token remains illiquid regardless of the technical infrastructure surrounding it.

Is tokenized real estate regulated?

In many jurisdictions, tokenized structures may fall under securities or financial regulation depending on how the tokens are structured and offered. Regulatory frameworks such as MiCA in the EU and VARA in the UAE provide specific oversight for digital asset activities. Regulatory classification must be determined before token issuance, not after.

Conclusion

Evaluating the benefits and risks of tokenized real estate requires recognizing that infrastructure modernization introduces both opportunity and complexity simultaneously. The coat check ticket is lightweight and tradeable. But its value depends entirely on the integrity of the coat check stand behind it.

The potential benefits are real: fractional accessibility, operational efficiency, ledger-based transparency, and secondary market infrastructure. The material risks are equally real: regulatory uncertainty, Insolvency Remoteness gaps, smart contract vulnerabilities, the Oracle Problem, Exit Liquidity limitations, platform dependency, and traditional property market exposure.

Tokenization enhances infrastructure. It does not eliminate legal, regulatory, or market risk. Balanced evaluation and structured due diligence using the Red Flag and Green Flag framework remain essential before engaging with any tokenized real estate structure. One red flag in the foundation layer is enough reason to pause and investigate further.

Sources and Regulatory References

- Bank for International Settlements (BIS): https://www.bis.org

- Organisation for Economic Co-operation and Development (OECD): https://www.oecd.org

- U.S. Securities and Exchange Commission (SEC): https://www.sec.gov

- European Securities and Markets Authority (ESMA): https://www.esma.europa.eu

Educational Disclaimer

This article is provided for educational purposes only and does not constitute financial, legal, or investment advice. Regulatory treatment of tokenized real estate varies by jurisdiction and asset classification. Professional legal consultation should be obtained before engaging with any tokenized property structure.

Last updated: March 2026

Explore Tokenized Real Estate

- Tokenized Real Estate Explained

- Fractional Ownership in Tokenized Real Estate

- Legal Structures Behind Tokenized Real Estate

- How Tokenized Real Estate Works Compared to Traditional Property Investment

- What Types of Properties Can Be Tokenized

- Benefits and Risks of RWA Tokenization (cluster)

- Why Compliance Matters in Tokenized Finance (cross-pillar)

- What Is Proof of Reserve (cross-pillar)

- On-Chain Transparency Explained (cross-pillar)

- Real-World Assets Hub

{kind=link}