Are Real-World Assets the Same as Physical Assets? A Complete Educational Clarification

This article is part of the broader Real-World Assets educational framework, answering whether real-world assets are the same as physical assets and explaining the structural distinction between material existence and legally recognized ownership in financial systems.

Educational Notice

This article is provided for informational and educational purposes only. It does not constitute financial, legal, or investment advice. Regulatory treatment of asset classification varies by jurisdiction.

Introduction

Are real-world assets the same as physical assets? This question comes up frequently because many real-world assets do exist in tangible form. A building is physical. Gold is physical. But the question of whether real-world assets are the same as physical assets requires a more precise answer, because the two terms operate at different levels of classification.

Physical assets describe the material nature of an asset: whether it can be touched, measured, and physically located. Real-world assets describe the legal and economic classification of ownership tied to enforceable economic value. These are not the same thing. One describes what something is made of. The other describes whether it exists within a legally recognized ownership framework that financial systems can engage with.

Understanding whether real-world assets are the same as physical assets is essential for interpreting asset classification within financial systems, tokenization frameworks, and regulatory structures. It also matters for understanding what tokenization can and cannot represent, and why the RWA (Real-World Asset) category is broader than most people initially assume.

If you are new to the broader concept, start here:

- What Are Real-World Assets?

- Examples of Real-World Assets Used in Tokenization

- What Is Asset Tokenization? A Beginner-Friendly Explanation

In Simple Terms: Are Real-World Assets the Same as Physical Assets?

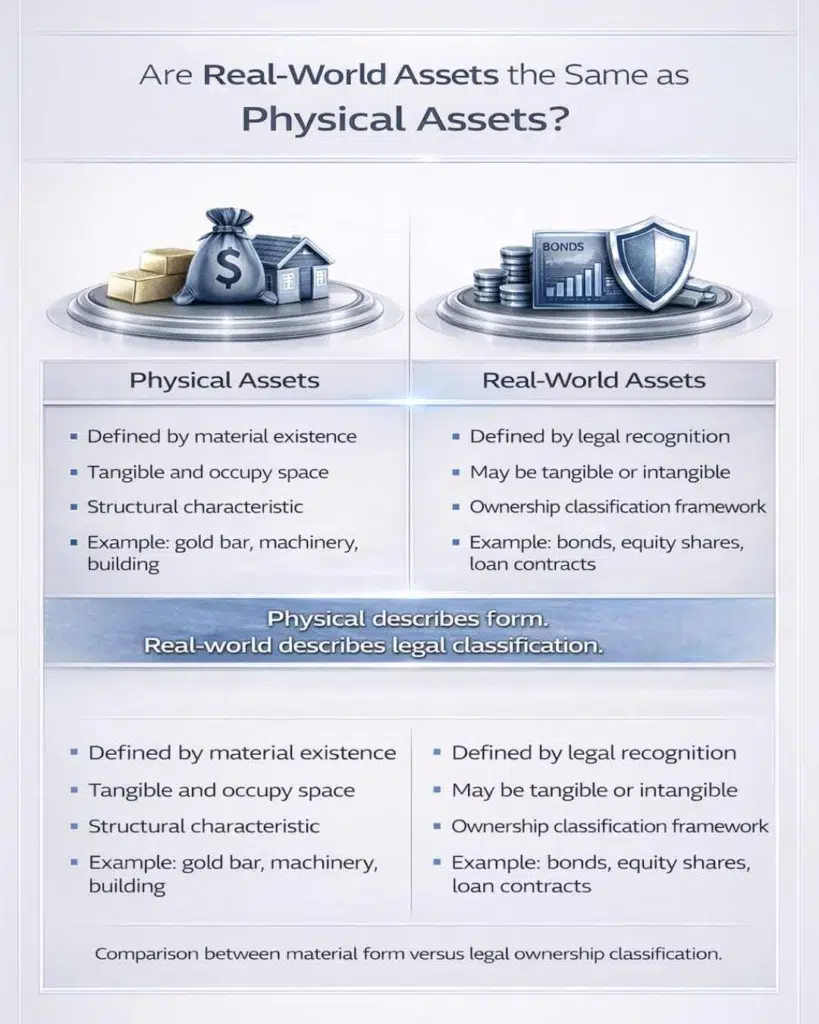

No. Real-world assets and physical assets are not the same. Physical assets refer to assets that exist in material, tangible form. Real-world assets refer to assets that are legally recognized and economically enforceable within financial systems. The professional distinction is Tangible vs Intangible: Tangible assets have physical presence you can measure and touch. Intangible assets (such as bonds, patents, royalties, and equity shares) have no physical form but carry legally enforceable economic rights that qualify them fully as real-world assets.

All physical (Tangible) assets can qualify as real-world assets if they have legally recognized ownership. However, not all real-world assets are physical. A government bond, a music royalty contract, or a software patent is not tangible, but each is unquestionably a real-world asset because it represents a legally enforceable claim to real economic value.

Are Real-World Assets the Same as Physical Assets? Key Differences

Are real-world assets the same as physical assets? The table below maps the core structural differences between the two classifications.

| Physical Assets | Real-World Assets |

|---|---|

| Defined by material, tangible existence | Defined by legal and economic recognition |

| Tangible: can be touched, measured, located | May be Tangible or Intangible |

| Structural material characteristic | Ownership classification framework |

| Example: gold bar, building, machinery | Example: bonds, equity shares, patents, property rights |

| Focuses on material form layer | Focuses on legally enforceable ownership |

| Often lower Counterparty Risk if held directly | Intangible RWAs carry Counterparty Risk from issuer |

This distinction highlights why are real-world assets the same as physical assets is a question worth answering carefully. The two terms are related but not interchangeable.

What Are Physical Assets?

Physical assets are Tangible assets: assets that exist in material form, occupy physical space, and can be measured, inspected, and located. Their defining characteristic is physical presence. Examples include real estate properties, machinery and equipment, gold bars and other commodities, vehicles, and infrastructure facilities.

Physical existence alone, however, does not determine how an asset is classified within financial systems. The material object and the legally recognized ownership of that object are treated as separate components. You can have a physical gold bar with no documented ownership. In that case, the gold is physically present but may not function as an asset within a regulated financial system without legally recognized title. Physical assets represent the material layer of asset structure. Legal recognition is what makes them financially functional.

Physical assets also typically carry lower Counterparty Risk (the risk that the other party in a transaction or ownership structure fails to deliver) than intangible financial instruments. If you hold a gold bar directly in a secure vault, you own it regardless of what happens to the institution that sold it to you. The gold is yours. There is no issuer that can default. Contrast this with a bond: if the bond issuer defaults, your claim to future cash flow may be impaired even though the bond itself represented a legally recognized right. This Counterparty Risk difference is one of the key reasons physical assets are treated differently in portfolio construction than purely intangible financial instruments.

What Are Real-World Assets?

Real-world assets (RWAs) represent assets that exist within legally recognized ownership and economic frameworks outside purely digital-native systems. Their defining characteristic is enforceable ownership tied to real economic value, not physical form. The professional term for the broader category is Financial Instruments when the focus is on legal claims to future cash flow: assets that represent a right to receive economic value regardless of whether they are backed by a physical building or a digital software patent.

Examples of real-world assets include both Tangible and Intangible categories. Tangible RWAs: property ownership rights, commodity holdings, infrastructure assets. Intangible RWAs: government and corporate bonds (representing legal claims to future interest and principal payments), corporate equity shares (representing ownership rights in a company without physical form), intellectual property (IP) such as patents, trademarks, and copyrights, royalty agreements, loan contracts, and revenue-generating agreements. All of these are real-world assets because they represent legally enforceable economic rights in the world outside blockchain systems.

According to the Bank for International Settlements (BIS), financial systems rely on legally enforceable ownership claims tied to real economic value to maintain stability and capital allocation efficiency. Are real-world assets the same as physical assets? No, because this definition encompasses far more than physical objects.

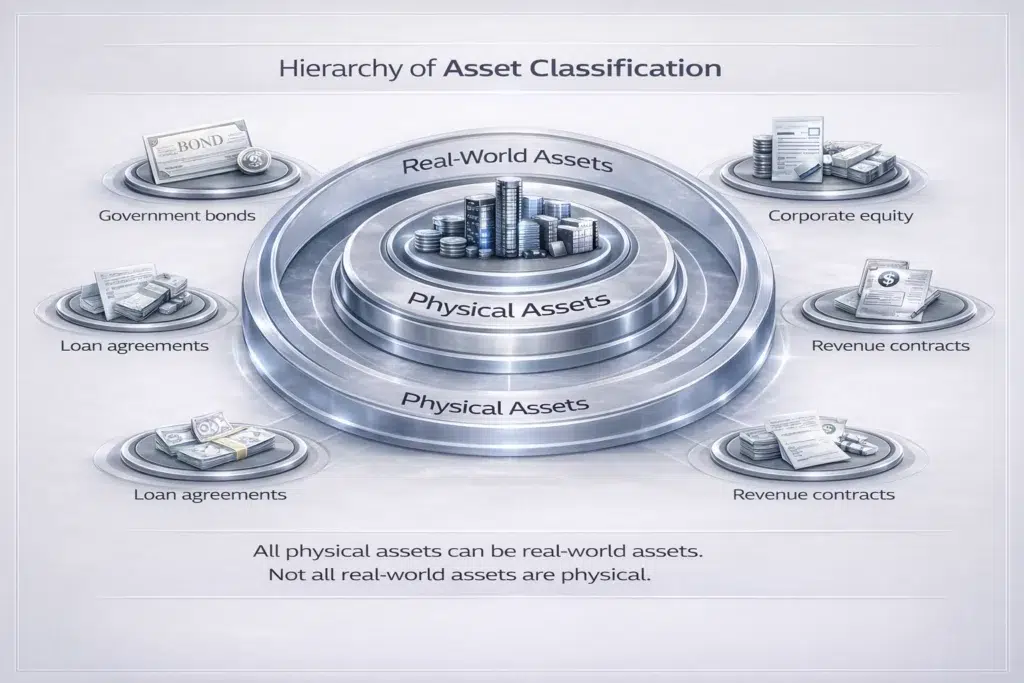

Physical Assets Are a Subset of Real-World Assets

The relationship between physical assets and real-world assets is hierarchical, not equivalent. Are real-world assets the same as physical assets? No: physical assets are one category within the broader real-world assets classification, not the full definition of it.

All physical (Tangible) assets qualify as real-world assets if:

- Ownership is legally recognized within a jurisdiction

- The asset exists within enforceable legal frameworks that allow title to be transferred

- It can be integrated into financial systems for valuation, transfer, and investment

However, many real-world assets do not have physical form at all. A government bond is a real-world asset but not a physical asset. A share in a company represents ownership rights, not material existence. A music royalty agreement is legally enforceable and economically valuable but entirely intangible. A software patent grants its holder rights to future licensing revenue without any physical counterpart. In every case, these are real-world assets because ownership is legally recognized and economically enforceable, regardless of whether anything physical backs them.

This distinction demonstrates that real-world asset classification is based on ownership recognition and legal enforceability, not material form.

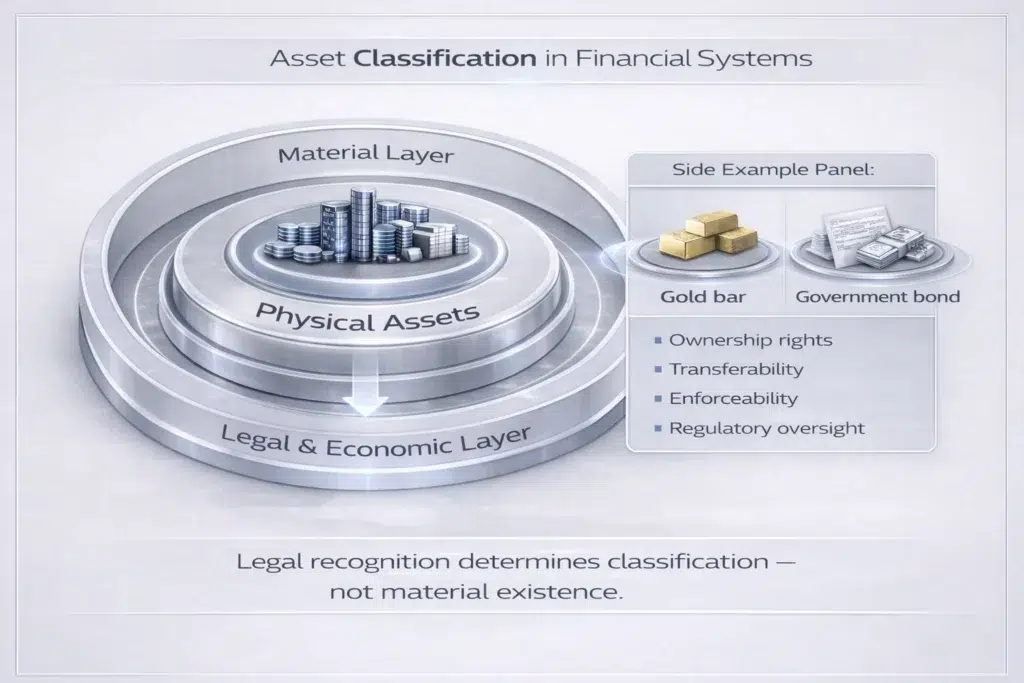

Applied Example: Gold Bar vs Government Bond

Two assets illustrate the distinction clearly. Consider a gold bar and a government bond.

The gold bar is a Physical (Tangible) asset: it exists in material form and can be touched, weighed, and stored. It is also a real-world asset if ownership is legally recognized through a documented title or custody arrangement. The holder of the gold bar directly controls it. Counterparty Risk is low: if the custodian institution fails, the gold bar remains physically present and the holder’s legal title to it is unaffected by the institution’s insolvency (assuming an Insolvency-Remote custody structure).

The government bond is not a physical asset at all. It is entirely intangible: there is no material object. Yet it is clearly a real-world asset because it represents a legally enforceable claim to future interest payments and principal repayment from a government issuer. The bond qualifies as a real-world asset because it represents ownership of a contractual economic right, not because anything physical backs it. The bond does carry Counterparty Risk: if the government defaults or restructures, the cash flow promised by the bond may not be fully delivered. The holder cannot simply “pick up” the bond’s value the way a gold holder can pick up their gold bar.

Are real-world assets the same as physical assets? This example demonstrates why they are not. One category is defined by material form. The other is defined by legal and economic recognition. Both assets in this example are real-world assets. Only one is a physical asset.

Why Physical Form Alone Does Not Define Asset Classification

Physical form describes structural characteristics. Asset classification in financial systems depends on legal and economic recognition, not material presence. An object may exist physically but cannot function as an asset within financial systems unless ownership is legally recognized. A gold bar buried in an unmarked field with no documented ownership may be physically present, but it functions outside any financial system until legal title is established.

Conversely, ownership rights may exist independently of physical form and still qualify fully as real-world assets. A software patent represents no physical object, but it grants its holder legally enforceable rights to licensing revenue that can be transferred, sold, and tokenized using exactly the same on-chain infrastructure as a physical building.

This is what practitioners mean by Asset Class Neutrality: tokenization is indifferent to whether the underlying asset is Tangible or Intangible. The process of representing ownership rights on blockchain follows the same structural framework whether the asset is a gold bar, a commercial building, a music royalty stream, or a corporate bond. The legal recognition layer is what matters. The physical form of the underlying asset is operationally irrelevant to the tokenization mechanism.

The OECD (Organisation for Economic Co-operation and Development) has noted that financial systems are built upon legally enforceable ownership structures that enable assets to be transferred, valued, and integrated into economic activity. This reinforces that ownership recognition, not physical existence, defines real-world asset classification and answers why are real-world assets the same as physical assets with a clear no.

Legal Frameworks Define Real-World Asset Classification

Asset classification within financial systems is governed by legal frameworks that define ownership rights, transferability, enforceability, and regulatory oversight. These frameworks do not require an asset to be physical. They require ownership to be legally recognized and economically enforceable.

Asset classification under these frameworks includes:

- Ownership rights: whether legal title or contractual rights to economic benefits are formally established

- Transferability: whether ownership can be legally transferred to another party

- Enforceability: whether courts and regulatory systems recognize and protect the ownership claim

- Regulatory oversight: whether the asset falls within securities law, property law, or other regulatory frameworks

The U.S. Securities and Exchange Commission (SEC) emphasizes that securities ownership is defined by legal enforceability rather than physical characteristics. A bond is a security not because of physical form but because it represents a legally enforceable financial claim. Are real-world assets the same as physical assets in this legal context? No: the legal framework classifies assets by their ownership structure, not their material properties.

Digital Infrastructure and Ownership Recording

Modern financial systems increasingly record ownership digitally. Blockchain-based tokenization extends this further by creating programmable digital representations of ownership rights. But digital representation does not redefine classification. Whether a tokenized asset is classified as physical or real-world depends on the underlying legal ownership, not on how the digital record is maintained.

Are real-world assets the same as physical assets in the context of tokenization? No, and this matters directly for understanding what can be tokenized. Tokenization can represent ownership rights to a physical building, a gold bar, a corporate bond, a music royalty stream, a carbon credit, or a software patent. All of these are real-world assets. Only some are physical assets. The tokenization mechanism is Asset Class Neutral: it operates identically regardless of whether the underlying asset is Tangible or Intangible. For technical explanation of ownership recording mechanisms, see How Real-World Assets Are Represented on Blockchain.

Why This Distinction Matters

Understanding whether real-world assets are the same as physical assets is not merely academic. It has practical consequences for classification, analysis, and regulatory interpretation. Are real-world assets the same as physical assets in every context? No, and misunderstanding this creates real problems in several areas.

It clarifies asset classification frameworks for financial analysis and portfolio construction. It prevents confusion in tokenization discussions where people assume only physical objects can be tokenized. It separates material structure from legal ownership, which matters for understanding Counterparty Risk differences between Tangible and Intangible holdings. It improves regulatory interpretation by making clear that RWA regulation covers intangible Financial Instruments as well as physical property.

Common Misunderstandings

Three misconceptions regularly arise when people first encounter the question of whether real-world assets are the same as physical assets.

The first misconception is that real-world assets must be physical. The reality is that real-world assets are defined by ownership recognition and legal enforceability, not physical form. Bonds, patents, royalties, and equity shares are all real-world assets despite being entirely intangible.

The second misconception is that physical assets and real-world assets are identical categories. The reality is that physical assets are one Tangible subset of the broader real-world assets classification. Real-world assets include both Tangible and Intangible categories, making it a significantly larger set.

The third misconception is that physical existence determines financial classification. The reality is that legal enforceability determines classification. An object may be physically present but legally unrecognized in financial systems. Conversely, an intangible contractual right may be fully enforceable and highly valuable within those same systems.

FAQ: Are Real-World Assets the Same as Physical Assets?

Are real-world assets the same as physical assets?

No. Physical assets describe material, Tangible existence. Real-world assets describe legally recognized ownership structures tied to real economic value. Physical assets are one subset of real-world assets. Many real-world assets are entirely intangible.

Are all physical assets real-world assets?

Yes, if they exist within legally enforceable ownership frameworks. A gold bar with documented title and legal recognition is both a physical asset and a real-world asset. An undocumented physical object with no legal ownership structure functions outside financial systems regardless of its physical presence.

Can a real-world asset exist without physical form?

Yes. Government bonds, corporate equity shares, patents, music royalties, and loan contracts are all real-world assets with no physical form. They are Intangible Financial Instruments: assets representing legally enforceable claims to future economic value. Are real-world assets the same as physical assets in these cases? Clearly not.

Why does this distinction matter in tokenization?

Tokenization represents ownership rights regardless of whether the underlying asset is Tangible or Intangible. This Asset Class Neutrality means the same on-chain infrastructure can represent a commercial building, a bond, or a software patent. Understanding that real-world assets include intangible Financial Instruments helps clarify the full scope of what tokenization can represent.

What is Counterparty Risk and how does it relate to this distinction?

Counterparty Risk is the risk that the other party in an ownership or payment arrangement fails to deliver. Physical assets held directly (such as gold in a segregated vault) typically carry lower Counterparty Risk because possession is independent of any third party’s solvency. Intangible RWAs like bonds carry Counterparty Risk because their value depends on the issuer honoring their contractual obligations. This risk difference is one reason physical and intangible real-world assets are treated differently in institutional portfolio frameworks.

Are digital-native assets real-world assets?

Digital-native assets such as cryptocurrencies are generally not classified as real-world assets because they are not tied to enforceable ownership of real economic resources outside the blockchain system itself. Their value derives from the blockchain protocol, not from a legal claim to a physical object or financial instrument in the real world.

Conclusion

Are real-world assets the same as physical assets? No. Real-world assets and physical assets are closely related but structurally distinct concepts. Physical assets refer to Tangible material existence. Real-world assets refer to legally recognized ownership tied to real economic value, encompassing both Tangible physical objects and Intangible Financial Instruments such as bonds, patents, royalties, and equity shares.

Physical assets represent one structural category within the broader real-world assets classification. The defining characteristic of real-world assets is not physical form but enforceable ownership within legal and financial systems. Are real-world assets the same as physical assets in a financial or regulatory context? No: classification depends on legal recognition, not material presence.

Understanding this distinction is essential for accurate asset classification, regulatory interpretation, and analysis of modern financial infrastructure, particularly as tokenization enables both Tangible and Intangible real-world assets to be represented on blockchain through the same Asset Class Neutral mechanism.

Sources and Regulatory References

- Bank for International Settlements (BIS): https://www.bis.org

- Organisation for Economic Co-operation and Development (OECD): https://www.oecd.org

- U.S. Securities and Exchange Commission (SEC): https://www.sec.gov

Educational Disclaimer

This article is provided for educational purposes only and does not constitute financial, legal, or investment advice. Regulatory treatment of asset classification varies by jurisdiction.

Last updated: March 2026

Explore Real-World Assets

- What Are Real-World Assets?

- Examples of Real-World Assets Used in Tokenization

- What Is Asset Tokenization? A Beginner-Friendly Explanation

- How Real-World Assets Are Represented on Blockchain

- Real-World Assets vs Digital Assets

- Real-World Asset Tokenization Explained (cluster)

- Benefits and Risks of RWA Tokenization (cluster)

- What Is Proof of Reserve (cross-pillar)

- Why Compliance Matters in Tokenized Finance (cross-pillar)

- Real-World Assets Hub

{kind=link}