AI vs Rule-Based Systems in Investment Platforms: 15 Critical Structured Differences

This article is part of the broader Investment Infrastructure educational framework, examining AI vs rule-based systems in investment platforms across fifteen structural differences including logic architecture, adaptability, false positive rates, explainability, maintenance costs, and the hybrid approach most modern platforms use today.

Educational Notice

This article is provided for informational and educational purposes only. It does not constitute legal, financial, or investment advice. The design and implementation of automated systems in financial infrastructure vary by jurisdiction and institutional framework. Professional consultation should be sought before relying on any financial technology system.

Introduction

Understanding AI vs rule-based systems in investment platforms requires examining how automated decision systems operate within modern financial infrastructure. Investment platforms increasingly rely on automated processes to analyze data, monitor transactions, detect risks, and support operational workflows. But not all automation is the same, and the differences between approaches matter enormously for governance, cost, performance, and regulatory compliance.

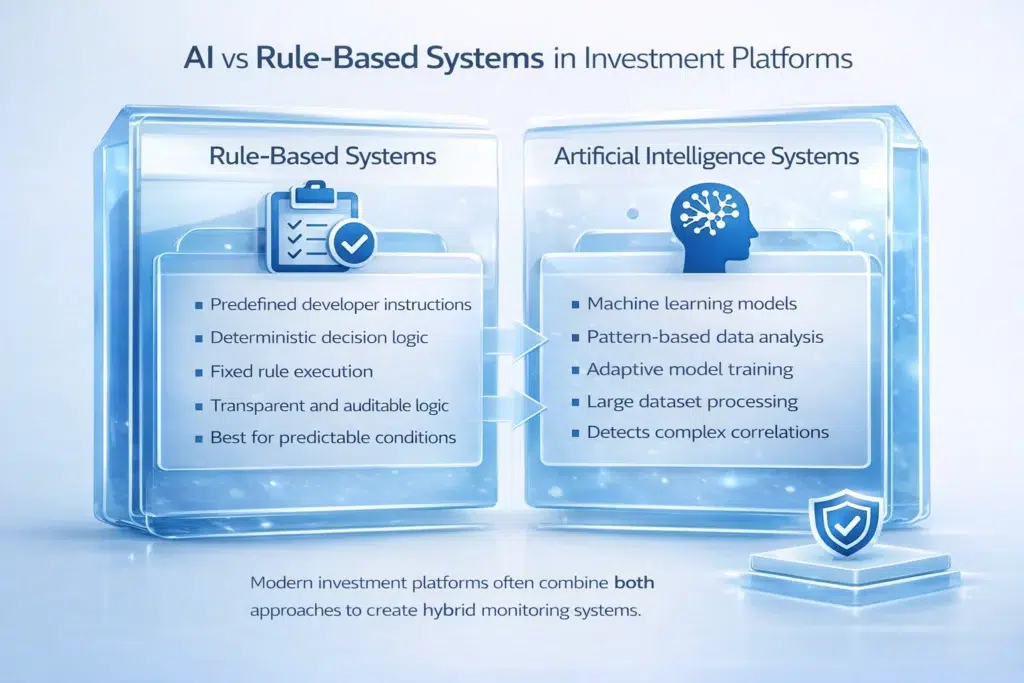

Historically, most financial systems relied on rule-based algorithms (automated systems that operate according to predefined instructions written by developers, where each rule determines exactly how the system should respond when specific conditions occur). These are Deterministic systems: given the same input, they always produce the same output. If X, then Y. Always.

As financial datasets became larger and more complex, artificial intelligence began playing a growing role. AI systems can analyze large volumes of financial information and detect patterns through Probabilistic models (systems that generate outputs based on statistical relationships learned from data rather than fixed rules, meaning the same input may produce different outputs depending on context and learned patterns). Both approaches have specific strengths, specific weaknesses, and specific appropriate use cases within modern financial infrastructure.

Understanding AI vs rule-based systems in investment platforms helps clarify how financial infrastructure processes complex information. For the broader infrastructure environment where these systems operate, see the Investment Infrastructure pillar. For how AI technologies support modern financial platforms across 14 specific applications, see How AI Is Used in Investment Infrastructure.

The Bank for International Settlements (BIS), the IMF, and the OECD all examine how artificial intelligence and advanced analytics may influence financial stability and infrastructure design.

In Simple Terms: AI vs Rule-Based Systems in Investment Platforms

Here is the clearest way to think about AI vs rule-based systems in investment platforms. A rule-based system is like a Strict Recipe. The recipe says: add 2 eggs, 1 cup of flour, bake for 20 minutes. If you have no eggs, the system stops. It cannot adapt. It does exactly what the instructions say, no more and no less. It is perfectly reliable for the exact situation it was designed for. The moment you encounter an ingredient it wasn’t expecting, it fails.

An AI system is like a Professional Chef. The chef knows the concept of a cake. If there are no eggs, the chef might use applesauce instead, because they understand the underlying pattern of how a cake comes together. They can adapt to the ingredients (data) they have and still produce a good result. The chef’s knowledge is not stored as a list of rules. It is stored as deep pattern recognition built up from years of experience.

Most good bakeries (financial platforms) use both. They follow a strict recipe for the basics (rule-based systems handle compliance thresholds, fixed reporting, and stable deterministic processes) and let the Chef experiment with the specials (AI handles fraud detection, anomaly recognition, and complex pattern analysis where rigid rules would fail). This Hybrid Architecture is not a compromise. It is the optimal design for modern investment infrastructure.

Why Investment Platforms Use Automated Decision Systems

Financial markets generate enormous volumes of data every second. Transactions occur across exchanges, blockchain networks, and digital investment platforms continuously. Monitoring this information manually would be practically impossible at institutional scale. Automated systems allow financial infrastructure to analyze data continuously and respond to operational events in real time, monitoring transaction activity, market volatility, liquidity conditions, regulatory compliance signals, and cybersecurity threats simultaneously.

Some functions suit deterministic rule-based logic: a transaction over a fixed regulatory reporting threshold must always trigger a report, no exceptions. Other functions suit AI-based models: identifying whether a specific transaction pattern across a specific account is genuinely suspicious requires context that no fixed rule can fully capture. Understanding AI vs rule-based systems in investment platforms helps clarify which tool fits which function.

AI vs Rule-Based Systems in Investment Platforms: 15 Critical Differences

Difference 1: Logic Foundation

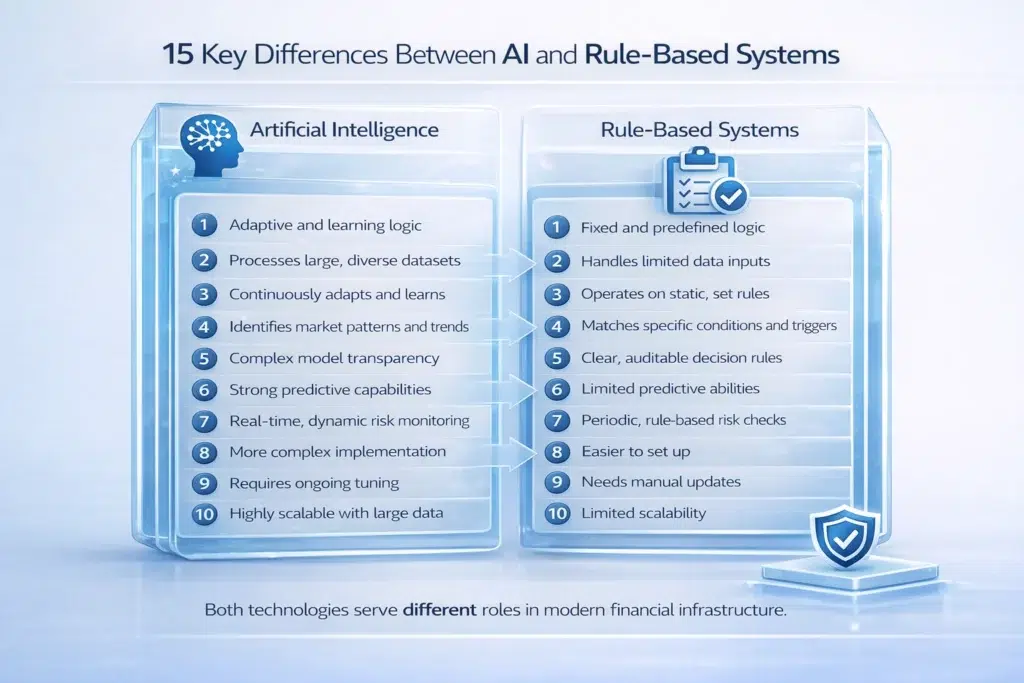

Rule-based systems operate on hard, Deterministic logic (if X, then Y: a specific condition always produces a specific result, with no variation). Every decision traces back to a specific instruction written by a developer. AI systems operate on Probabilistic logic (the system generates outputs based on patterns, correlations, and statistical likelihoods learned from data). The same input may produce slightly different outputs depending on context. In AI vs rule-based systems in investment platforms, this distinction is the foundation of every other difference: one system follows instructions, the other learns patterns.

Difference 2: Adaptability to Market Changes

Rule-based systems are Static: they cannot change themselves. A human developer must manually rewrite the code to update a rule when market conditions change, regulations evolve, or new fraud patterns emerge. AI systems are Dynamic: machine learning models (AI systems that improve their analytical accuracy by learning from new data) can adapt through retraining processes that incorporate new data automatically. In the AI vs rule-based systems in investment platforms comparison, this adaptability difference is particularly significant in fast-moving financial markets where conditions can shift dramatically within weeks.

Difference 3: Data Processing Capability

Rule-based systems typically process Structured Data only (neatly organized data in fixed formats, like spreadsheets or database tables with defined fields). AI systems can process Unstructured Data (information without a predefined format, such as news articles, social media sentiment, earnings call transcripts, satellite images of retail car parks, or behavioral patterns across account histories). This difference is one of the primary reasons AI systems are increasingly integrated into modern financial infrastructure: the most valuable signals are often found in data that rule-based systems cannot read.

Difference 4: Problem Solving Approach

Rule-based systems excel at Simple, Binary Problems (questions with a clear yes/no answer based on a fixed threshold): Is this trade over $10,000? YES or NO. AI systems excel at Complex, Gray-Area Problems (questions where context matters and the correct answer depends on patterns across multiple variables): Is this specific transaction unusual for this specific user’s historical behavior pattern? This difference defines where each approach belongs in AI vs rule-based systems in investment platforms design: use rules for binary thresholds, use AI for contextual judgment.

Difference 5: Anomaly Detection Method

Rule-based systems use Threshold-Based detection (they flash an alert only when a hard numerical limit is crossed, for example flagging any transaction above $5,000 regardless of who made it or why). AI systems use Behavioral-Based detection (they learn what “normal” looks like for each specific account, user, or system and only alert on meaningful deviations from that established pattern). In the AI vs rule-based systems in investment platforms comparison, behavioral detection is significantly more sophisticated: it can identify that a $200 transaction is suspicious for a specific account even though the same transaction would be completely normal for another.

Difference 6: False Positive Rates

This is one of the most operationally significant differences in AI vs rule-based systems in investment platforms. Rule-based systems generate High False Positive rates (alerts flagging legitimate activity as suspicious) because they apply the same thresholds to every account regardless of context. A rule that flags every transaction over $10,000 will flag a company’s regular vendor payment every single time, creating alert fatigue and wasting compliance resources on known-legitimate activity.

AI systems generate significantly Lower False Positive rates because they learn context. The system learns that a specific account regularly makes $50,000 payments to a specific vendor on the last Friday of each month. That payment pattern is normal for that account. The AI stops flagging it. This reduces Alert Fatigue (the phenomenon where compliance teams begin ignoring alerts because too many have proven unfounded, paradoxically making genuine risks less likely to be caught) and directs human attention toward genuinely anomalous signals. For the full governance context on AI monitoring systems, see What Role Does AI Play in Risk Management Infrastructure?

Difference 7: Scalability

Rule-based systems scale Linearly: adding more rules makes the system progressively slower, more complex, and harder to maintain. This is the Spaghetti Code problem (a state where thousands of interdependent rules accumulate over years, creating a system so tangled that changing one rule unexpectedly breaks several others). AI systems scale Exponentially: models generally become more accurate and efficient as they process more data, without the same compounding complexity cost. In AI vs rule-based systems in investment platforms, this scalability difference becomes decisive for large institutions managing millions of daily transactions.

Difference 8: Transparency and Explainability

Rule-based systems are White Box systems (systems where every decision can be instantly explained by pointing to a specific rule: “This transaction was flagged because it triggered Rule 47: amount exceeds $10,000 threshold”). The logic is fully transparent, auditable, and explainable to regulators without technical expertise.

Standard AI systems are often Black Box systems (systems where the model produces outputs through complex internal computations that cannot be easily explained in human-readable terms). The EU AI Act (the world’s first comprehensive AI regulation) specifically classifies financial services AI as High-Risk, requiring explainability. This creates demand for Explainable AI (XAI), also called White Box or Glass Box AI (AI systems specifically designed to show which data factors drove each decision, making the logic transparent and auditable). In AI vs rule-based systems in investment platforms, the governance implication is clear: rule-based systems are inherently explainable, while AI systems require specific XAI design to meet regulatory standards. For the full transparency analysis, see Why AI Requires Transparency in Financial Infrastructure.

Difference 9: Maintenance and Code Decay

Rule-based systems require Manual and Costly maintenance: developer time to add new rules, update existing ones when regulations change, and retire outdated ones when market conditions evolve. Over time, this creates Code Decay (the gradual deterioration of a rule-based system’s performance and manageability as old rules accumulate, conflict with newer rules, and reflect market conditions that no longer exist). A financial institution operating for 20 years may have accumulated thousands of rules, many of which are outdated, conflicting, or redundant but too risky to remove without extensive testing.

AI systems require Continuous Training (periodic retraining of the model on new data to maintain accuracy) but the model maintains its own decision logic as it learns. There is no accumulating rule library to manage. The AI vs rule-based systems in investment platforms maintenance comparison is one of the most compelling arguments for AI adoption from a total cost perspective: the long-term operational cost of maintaining a large rule engine can significantly exceed the cost of training and monitoring an AI model.

Difference 10: Innovation Speed

Rule-based systems evolve slowly, limited by the speed at which human analysts can identify new conditions and developers can write, test, and deploy new rules. AI systems evolve faster, limited primarily by data availability and computational power rather than human coding capacity. In rapidly evolving financial environments, AI vs rule-based systems in investment platforms innovation speed can determine whether an institution detects emerging fraud patterns in weeks or months.

Difference 11: Risk Profile

Rule-based systems carry a Predictable risk profile: institutions know exactly what Rules 1 through 500 will do in any given situation. The risks are defined, documented, and auditable. AI systems carry an Uncertain risk profile: new, unknown risks can emerge from unexpected model behavior, including learning biased patterns from historical data, generating hallucinations (fabricated outputs confidently presented as fact), or producing outputs that degrade as market conditions drift from training data. In AI vs rule-based systems in investment platforms, the risk profile difference means rule-based systems are often preferred for compliance-critical functions where predictability is legally required. For a complete analysis, see Limitations of AI in Investment Infrastructure Explained.

Difference 12: Human Capital Requirements

Rule-based systems are Developer-Intensive: they require software engineers to build, maintain, and update the rule engine continuously. AI systems are Data Scientist-Intensive: they require data experts to build training datasets, validate model performance, monitor for drift, and retrain models periodically. The AI vs rule-based systems in investment platforms human capital comparison matters for institutional planning: switching from rule-based to AI-based systems often requires hiring different skills, not simply retraining existing staff.

Difference 13: Institutional Use Cases

Rule-based systems remain the standard for Legacy Infrastructure applications (basic compliance monitoring, fixed regulatory reporting, stable deterministic processes where every decision must be fully traceable to a specific rule). AI systems are increasingly used for Modern Infrastructure applications: fraud detection at scale, sentiment analysis, predictive risk modeling, behavioral anomaly detection, and ESG data processing. In AI vs rule-based systems in investment platforms, the institutional use case distinction guides which technology belongs in which part of the platform architecture.

Difference 14: Security Monitoring

AI systems can analyze system behavior patterns continuously and detect Network Anomalies (deviations from normal traffic, access, or interaction patterns that may indicate unauthorized access or active intrusions) that rule-based systems would miss entirely. Rule-based systems detect security risks only when predefined conditions are triggered: they are effective against known attack patterns but blind to novel ones. In AI vs rule-based systems in investment platforms, this security difference is becoming increasingly significant as cyber threats evolve faster than rule updates can keep pace with.

Difference 15: Integration With Blockchain Infrastructure

AI models can analyze blockchain transaction activity and detect complex behavioral patterns across decentralized financial systems that fixed rules cannot identify. Blockchain Transparency mechanisms such as Proof of Reserve systems (verification mechanisms that confirm the real-world assets backing on-chain claims actually exist) complement AI monitoring by providing verifiable underlying records. See What Is Proof of Reserve in Blockchain Systems? and On-Chain Transparency Explained. In AI vs rule-based systems in investment platforms, blockchain integration capability is an increasingly important differentiator as tokenized financial infrastructure expands.

Full Comparison: AI vs Rule-Based Systems in Investment Platforms

| Feature | Rule-Based Systems (The Strict Recipe) | AI Systems (The Professional Chef) |

|---|---|---|

| Logic Foundation | Deterministic: hard If X, then Y rules created by a human | Probabilistic: patterns and statistical likelihoods learned from data |

| Adaptability | Static: humans must manually rewrite code to update rules | Dynamic: model automatically updates as new data flows in |

| Data Processing | Structured data only (spreadsheets, fixed database tables) | Structured and unstructured data (news, sentiment, behavioral signals) |

| Problem Solving | Simple binary problems: Is this trade over $10,000? YES/NO | Complex gray-area problems: Is this unusual for this specific user? |

| Anomaly Detection | Threshold-Based: alerts only when a hard limit is crossed | Behavioral-Based: alerts on deviation from learned normal patterns |

| False Positives | High: flags every large vendor payment regardless of context | Low: learns to distinguish fraud signals from normal business activity |

| Scalability | Linear: more rules create spaghetti code complexity | Exponential: models become more accurate with more data |

| Transparency | White Box: every decision explained by pointing to a specific rule | Black Box (standard) / White Box (XAI): requires Explainable AI design |

| Maintenance | Manual and costly: constant developer time, Code Decay over years | Automated retraining: model maintains decision logic itself |

| Innovation Speed | Slow: limited by human analysis and coding speed | Fast: limited only by data availability and computing power |

| Risk Profile | Predictable: known risks from Rules 1-500 are fully documented | Uncertain: new risks can emerge from bias, drift, or hallucinations |

| Human Capital | Developer-intensive: needs engineers to maintain the rule engine | Data scientist-intensive: needs experts to build and validate models |

| Institutional Use | Legacy: compliance thresholds, fixed reports, stable processes | Modern: fraud detection, sentiment analysis, predictive modeling |

| Code Decay | High: old rules accumulate and clash, system becomes unmanageable | Low: model stays current through retraining on new data |

| Best Used For | Deterministic reliability: irreversible logic, fixed compliance rules | Probabilistic flexibility: complex environments, pattern detection |

The Hybrid Architecture: Why Most Platforms Use Both

A central finding in AI vs rule-based systems in investment platforms is that the question is rarely either/or. Most modern financial platforms combine both approaches in a Hybrid Architecture (a system design that uses rule-based logic for deterministic, compliance-critical functions and AI models for complex pattern recognition and anomaly detection). The recipe handles the basics reliably. The Chef handles the situations the recipe never anticipated.

Rule-based systems handle regulatory reporting thresholds, fixed compliance checkpoints, and stable deterministic processes where every decision must be fully traceable and explainable. AI systems handle fraud detection, behavioral anomaly monitoring, market volatility pattern recognition, and predictive risk analytics where contextual intelligence outperforms rigid rules. Together, they create financial infrastructure that is both reliably compliant and adaptively intelligent.

Why Understanding AI vs Rule-Based Systems in Investment Platforms Matters

Understanding AI vs rule-based systems in investment platforms helps financial institutions evaluate the design of automated infrastructure systems. Infrastructure architecture influences operational stability, financial transparency, risk monitoring capabilities, regulatory compliance integration, and infrastructure security. Financial institutions must carefully evaluate which technologies are appropriate for specific operational functions rather than treating AI as a universal replacement for all rule-based systems.

Institutional Perspective

Institutions evaluating automated financial infrastructure in the context of AI vs rule-based systems in investment platforms typically consider transparency of system logic, governance frameworks, infrastructure reliability, regulatory compliance integration, and data quality and monitoring. International financial institutions continue studying how artificial intelligence may influence financial markets and infrastructure design. The BIS, IMF, and OECD all provide relevant research and policy discussions on these topics.

Frequently Asked Questions

What is the main difference between AI and rule-based systems in investment platforms?

The core difference in AI vs rule-based systems in investment platforms is the logic architecture. Rule-based systems are Deterministic (if X, then Y, always) and follow predefined instructions written by developers. AI systems are Probabilistic (they generate outputs based on statistical patterns learned from data) and can adapt to new situations that their rules never anticipated. Rule-based systems are like a Strict Recipe. AI systems are like a Professional Chef who understands the underlying pattern.

Why do AI systems have lower false positive rates than rule-based systems?

In AI vs rule-based systems in investment platforms, false positive rates differ because of how each system detects anomalies. Rule-based systems use Threshold-Based detection: any transaction over a fixed limit triggers an alert, regardless of context. AI systems use Behavioral-Based detection: they learn what normal looks like for each specific account and only alert on meaningful deviations. This means AI learns that a company’s regular $50,000 vendor payment is not fraud, while a rule-based system would flag it every single time.

What is Explainable AI (XAI) and why does it matter in this comparison?

Explainable AI (XAI), also called White Box or Glass Box AI, refers to AI systems specifically designed to show which data factors drove each decision, making the logic transparent and auditable. In AI vs rule-based systems in investment platforms, XAI bridges the explainability gap: rule-based systems are inherently explainable (point to the rule), while standard AI is a Black Box. The EU AI Act requires explainability for financial services AI, making XAI design a regulatory requirement rather than an optional feature.

What is Code Decay in rule-based systems?

Code Decay is the gradual deterioration of a rule-based system’s performance and manageability as old rules accumulate, conflict with newer rules, and reflect market conditions that no longer exist. A financial institution operating for 20 years may have thousands of rules, many outdated or conflicting but too risky to remove. In AI vs rule-based systems in investment platforms, code decay is one of the strongest arguments for AI adoption: AI models retrain on new data rather than accumulating a library of aging rules.

Do investment platforms use both AI and rule-based systems?

Yes. Most modern platforms use a Hybrid Architecture that combines both. Rule-based systems handle compliance thresholds, fixed regulatory reporting, and stable deterministic processes. AI systems handle fraud detection, behavioral anomaly monitoring, predictive analytics, and complex pattern recognition. Understanding AI vs rule-based systems in investment platforms helps clarify which tool belongs in which function rather than treating the two approaches as mutually exclusive.

Why do regulators monitor AI in financial systems?

Regulators monitor AI systems to ensure transparency, accountability, and risk management within financial infrastructure. The EU AI Act classifies AI in financial services as High-Risk, requiring documentation, explainability, and human oversight. In AI vs rule-based systems in investment platforms, this regulatory scrutiny applies primarily to AI because rule-based systems are inherently auditable (every decision traces to a specific rule), while standard AI Black Box systems require specific XAI design to meet the same auditability standard.

Conclusion

Understanding AI vs rule-based systems in investment platforms clarifies how modern financial infrastructure processes data and supports automated decision-making. Rule-based systems provide Deterministic Reliability: predictable execution based on predefined instructions, fully auditable, White Box by design, best for compliance-critical functions where every decision must trace to a specific rule. AI systems provide Probabilistic Flexibility: advanced analytical capabilities that interpret large datasets, detect complex behavioral patterns, reduce false positives, and adapt to changing market conditions, at the cost of requiring XAI design for regulatory compliance and active monitoring for model drift and bias.

Most modern financial platforms combine both approaches in a Hybrid Architecture. The Strict Recipe handles the basics with iron reliability. The Professional Chef handles the complex situations the recipe could never anticipate. Together, they create financial infrastructure that is both deterministically compliant and adaptively intelligent. Understanding AI vs rule-based systems in investment platforms is the foundation for building and evaluating any modern automated financial system.

Sources and Regulatory References

- Bank for International Settlements (BIS): https://www.bis.org

- International Monetary Fund (IMF): https://www.imf.org

- Organisation for Economic Co-operation and Development (OECD): https://www.oecd.org

Educational Disclaimer

This article is provided for educational purposes only and does not constitute legal, financial, or investment advice. The design and implementation of automated systems in financial infrastructure vary by jurisdiction and institutional framework. Professional consultation should be sought before relying on any financial technology system.

Last updated: March 2026

Explore AI in Investment Infrastructure

- AI in Investment Infrastructure Explained

- How AI Is Used in Investment Infrastructure

- What Role Does AI Play in Risk Management Infrastructure?

- Limitations of AI in Investment Infrastructure Explained

- Why AI Requires Transparency in Financial Infrastructure

- On-Chain Transparency Explained (cross-pillar)

- Transparency Reduces Risk in Tokenized Assets (cross-pillar)

- Why Compliance Matters in Tokenized Finance (cross-pillar)

- How Regulation Improves Transparency in Tokenized Finance (cross-pillar)

- Investment Infrastructure Hub

{kind=link}