Which Crypto Activities Are Covered Under MiCA Regulation? 14 Critical Structured Areas

This article is part of the broader Regulations and Compliance educational framework, examining how MiCA defines the regulatory perimeter for digital asset activities within the European Union.

Introduction

Which crypto activities are covered under MiCA regulation? This is the first question any business operating in EU digital asset markets must answer before designing its compliance architecture. The Markets in Crypto-Assets Regulation, known as MiCA (the European Union’s comprehensive legal framework that establishes uniform rules for issuing and trading crypto-assets across all 27 EU member states), creates a harmonized regulatory structure that is precise in both what it includes and what it deliberately leaves out. Operating inside the regulatory perimeter without authorization carries serious legal consequences, while misidentifying an unregulated activity as regulated creates unnecessary compliance burden.

MiCA defines its perimeter in two directions. It specifies what it covers, and it specifies what falls outside its scope. Both sides of that boundary matter equally. The regulation entered into full force on 30 December 2024, making the question of which crypto activities are covered under MiCA regulation directly actionable for firms already operating in or entering EU markets. For the official legislative text, see Regulation (EU) 2023/1114 on Markets in Crypto-Assets published in the Official Journal of the European Union.

Before examining the fourteen structured areas, one foundational distinction must be established: the difference between crypto-asset issuance and crypto-asset service provision. These two categories carry different authorization requirements, different disclosure obligations, and different supervisory relationships. Everything else in MiCA’s scope flows from this split.

For foundational context:

- What Is MiCA Regulation in Crypto?

- How MiCA Regulation Affects Tokenized Assets

- MiCA Regulation vs National Crypto Regulations in Europe

- Why Compliance Is Essential in Tokenized Finance

- Why Compliance Matters in Tokenized Finance

In Simple Terms: Which Crypto Activities Are Covered Under MiCA Regulation

MiCA regulates professional crypto activities performed within the EU by identifiable legal entities. The crypto activities covered under MiCA regulation include issuing certain crypto-assets, stablecoin issuance, operating trading platforms, providing custody services, exchange services, portfolio management, and advisory services. It does not regulate purely technological blockchain development or fully decentralized systems without an identifiable operator. The European Securities and Markets Authority (ESMA) publishes ongoing guidance and technical standards under MiCA that clarify how these categories apply in practice.

Two Core Categories Under MiCA

All regulated activity under MiCA falls into one of two categories: crypto-asset issuance or crypto-asset services. Issuance refers to creating and offering tokens to the public or admitting them to trading. Services refer to operating platforms or providing professional crypto-related financial services to clients. When asking which crypto activities are covered under MiCA regulation, the answer always traces back to one of these two parent categories. MiCA authorization requirements apply when these functions are carried out commercially within the European Union by an identifiable legal entity.

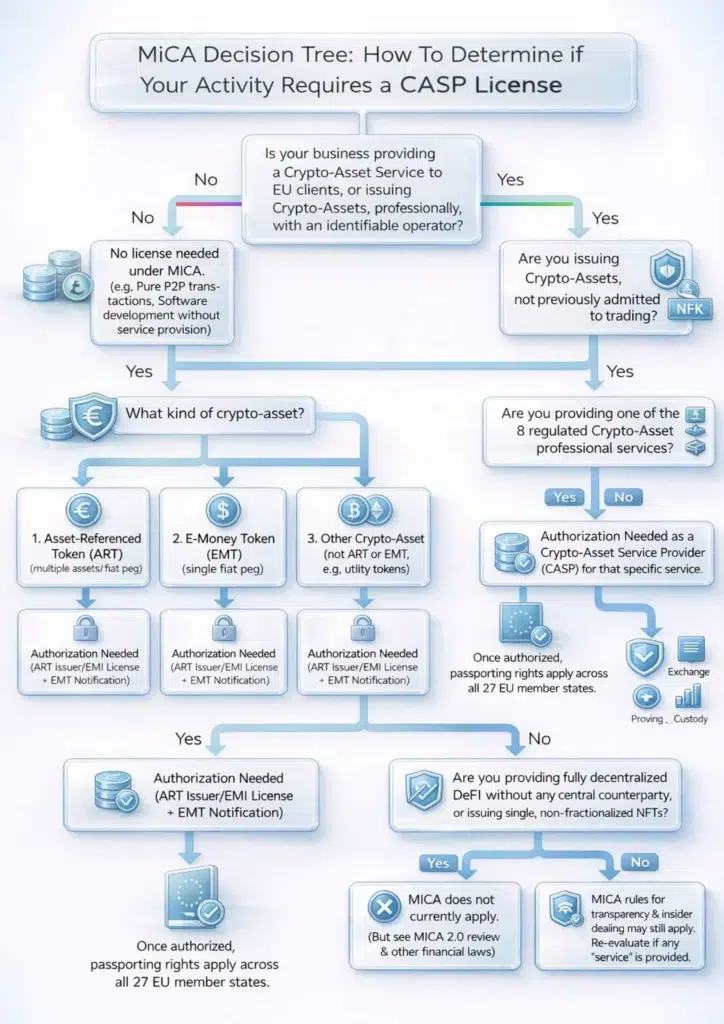

How to Classify Your Activity: Does Your Business Need a MiCA License?

Before examining each of the fourteen areas in detail, the diagram below maps the decision path for determining which crypto activities are covered under MiCA regulation, which fall under a different EU framework such as MiFID II (Markets in Financial Instruments Directive, the EU’s existing regulatory framework for traditional investment services), and which sit outside current regulation entirely. The EBA (European Banking Authority) has published its own MiCA guidelines and technical standards covering stablecoin classification and supervisory expectations, which complement this classification framework. Use the diagram as a first-pass classification tool before seeking formal legal advice.

A note on the diagram above: the substance over form rule (the regulatory principle that the legal treatment of an activity is determined by what it actually does in practice, not by how it is labelled or structured on paper) applies throughout this classification process. Which crypto activities are covered under MiCA regulation is ultimately a functional question, not a labelling question. Fully decentralized DeFi protocols (blockchain-based systems that operate through autonomous smart contracts without any identifiable central operator) and unique NFTs (Non-Fungible Tokens, unique digital assets representing ownership of a specific item) are currently outside MiCA scope. However, if an activity functions like a regulated service, EU regulators may treat it as one regardless of its label.

Stablecoin Classification: ARTs vs. EMTs

The distinction between Asset-Referenced Tokens and E-Money Tokens is the most technically complex part of MiCA for issuers and the most consequential for reserve management, redemption rights, and supervisory obligations. The two categories look similar on the surface but carry fundamentally different regulatory treatments.

An ART (Asset-Referenced Token, a crypto-asset whose value is pegged to a basket of multiple assets such as a mix of fiat currencies, commodities, or other crypto-assets) and an EMT (E-Money Token, a crypto-asset whose value is pegged to a single official fiat currency such as the euro or the US dollar) diverge significantly in how reserves must be held, how redemption rights work, and which supervisory authority oversees the issuer. The EBA has published detailed regulatory guidance on ART and EMT classification including draft technical standards on reserve asset requirements and redemption procedures.

| Dimension | ART (Asset-Referenced Token) | EMT (E-Money Token) |

|---|---|---|

| Peg Reference | Basket of currencies, commodities, or other crypto-assets | Single official fiat currency (e.g., EUR, USD) |

| Authorization | Authorization from national competent authority required | Must be issued by authorized credit institution or e-money institution |

| Reserve Requirements | Segregated reserve pool reflecting the basket composition | Funds held in secure, low-risk assets equal to tokens in circulation |

| Redemption Rights | Holders have right to redemption at any time at market value of reference assets | Holders have right to redeem at par value (face value) at any time |

| Interest Payments | Prohibited | Prohibited |

| Significant Issuer Threshold | Over 10 million holders or 5 billion EUR in market cap triggers enhanced EBA oversight | Same thresholds apply; classified as significant EMT under EBA supervision |

| Primary Regulator | National competent authority, EBA for significant issuers | National competent authority, EBA for significant issuers |

The practical implication of this distinction is significant. An issuer planning a euro-pegged stablecoin must obtain e-money institution authorization or partner with one. An issuer planning a basket-referenced token must apply directly to a national competent authority for ART authorization. Misclassifying between the two creates material compliance risk from the outset of the issuance process.

The CASP Passporting Advantage

One of the most strategically significant features of MiCA is the CASP passporting right. A CASP (Crypto-Asset Service Provider, a legal entity that is authorized to provide regulated crypto services under MiCA) that obtains authorization in any one EU member state gains the right to operate across all 27 EU member states without requiring separate national licenses in each jurisdiction.

This passporting mechanism (a legal right that allows a firm authorized in one EU country to provide regulated services in all other EU member states without additional national authorization) mirrors the framework established for traditional financial institutions under MiFID II and the Banking Directive. For digital asset businesses, it represents the single most compelling structural advantage of operating under MiCA rather than navigating 27 separate national frameworks.

The practical implications are substantial. A firm authorized as a CASP in France, Germany, or Ireland can serve clients across the entire EU single market from a single regulatory base. This reduces compliance costs, eliminates duplicate licensing processes, and creates a more predictable operational environment for scaling across EU markets. The choice of home member state for authorization is therefore a strategic decision, not merely an administrative one, since national competent authorities differ in their supervisory approach, processing times, and interpretive guidance. ESMA maintains a public register of authorized CASPs across EU member states as passporting notifications are processed.

The 14 Structured Areas: Which Crypto Activities Are Covered Under MiCA Regulation in Full

The following fourteen areas represent the complete answer to which crypto activities are covered under MiCA regulation. Each area carries its own authorization pathway, disclosure obligations, and supervisory relationship. The areas are organized in order of the two parent categories: issuance first, then service provision.

Area 1: Issuance of Asset-Referenced Tokens

ARTs reference multiple underlying assets. Issuers must obtain authorization from a national competent authority, publish a compliant whitepaper (a formal disclosure document containing standardized information about the token, the issuer, the rights of holders, and the risks involved), maintain a segregated reserve pool, implement governance systems meeting MiCA standards, and accept ongoing supervisory obligations. Large issuers exceeding defined thresholds face enhanced oversight from the EBA (European Banking Authority, the EU body responsible for supervising significant stablecoin issuers under MiCA).

Area 2: Issuance of E-Money Tokens

EMTs reference a single official currency. They must be issued by an authorized credit institution or licensed e-money institution. Reserve backing equivalent to all tokens in circulation is required, holders retain the right to redeem at par value at any time, and interest payments to holders are prohibited under MiCA. EMTs issued at scale face the same significant issuer thresholds as ARTs, triggering EBA supervision.

Area 3: Public Offering of Other Crypto-Assets

Crypto-assets that do not qualify as ARTs, EMTs, or financial instruments fall under MiCA’s third issuance category. Issuers conducting a public offering must produce a compliant whitepaper, provide clear risk disclosures, and ensure marketing communications are fair, clear, and not misleading. This category covers the broad landscape of utility tokens (crypto-assets that provide access to a product or service offered by the issuer rather than representing a financial investment) and similar instruments.

Area 4: Admission to Trading

When tokens are listed on a regulated trading platform, disclosure standards apply at the point of admission. Operators cannot list tokens without the required whitepaper and documentation. This area protects investors by ensuring that tokens available for trading on regulated venues have met minimum disclosure requirements before becoming accessible to the public.

Area 5: Operation of Trading Platforms

Operating a crypto exchange or trading venue requires CASP authorization. Operators must maintain governance controls, prevent conflicts of interest, monitor market integrity, and ensure operational resilience (the ability of a platform to continue functioning reliably even during adverse events such as technical failures or market stress). This area is one of the highest-volume authorization categories under MiCA given the number of existing exchange operators across the EU.

Area 6: Custody and Administration

Safeguarding client crypto-assets on behalf of third parties is a regulated activity. Custodians must protect holdings with appropriate cybersecurity safeguards, segregate client assets from their own corporate assets, and accept operational liability for losses resulting from failures in their custody infrastructure. Asset segregation under MiCA aligns with the broader principle that client funds must be protected even in the event of the custodian’s insolvency.

Area 7: Exchange of Crypto-Assets for Fiat Currency

Fiat-to-crypto and crypto-to-fiat exchange services require CASP authorization when provided commercially. Operators must implement AML (Anti-Money Laundering) procedures, KYC (Know Your Customer, the process of verifying the identity of clients before providing services) controls, and compliance systems meeting both MiCA and the EU’s Transfer of Funds Regulation requirements.

Area 8: Exchange of Crypto-Assets for Other Crypto-Assets

Crypto-to-crypto exchange services are regulated under MiCA when operated professionally and commercially. They require CASP licensing and compliance systems equivalent to those required for fiat exchange services. The distinction between a professional commercial exchange and a casual peer-to-peer transaction is relevant here: MiCA targets organized, systematic exchange activity, not isolated individual transactions.

Area 9: Execution of Orders on Behalf of Clients

Broker-style trade execution services, where a CASP executes crypto transactions on instruction from clients rather than on its own account, fall under MiCA. Requirements include acting in the client’s best interest, managing conflicts of interest transparently, and maintaining records of all executed orders. This area mirrors the best execution obligations familiar from MiFID II but applied within the crypto-specific framework of MiCA.

Area 10: Placing of Crypto-Assets

Placing (the distribution or sale of newly issued tokens on behalf of an issuer to investors, similar to an underwriting function in traditional capital markets) requires CASP authorization and must comply with disclosure standards and marketing transparency obligations. Firms that distribute tokens without being themselves the issuer must nonetheless meet MiCA’s authorization requirements if they are doing so commercially.

Area 11: Portfolio Management

Discretionary management of crypto-assets on behalf of clients (where the CASP makes investment decisions independently on behalf of the client) requires CASP authorization, governance frameworks, and risk management systems. This area brings crypto portfolio management into a regulatory structure comparable to the investment management rules under MiFID II, requiring firms to demonstrate suitability assessments and client mandate compliance.

Area 12: Advisory Services

Providing professional advice on crypto-assets requires CASP authorization. Advisors must make risk disclosures to clients, manage conflicts of interest, and hold the appropriate regulatory authorization. This area covers firms that provide research, recommendations, or personalized crypto investment guidance in a professional capacity.

Area 13: Transfer Services

Transfer services that facilitate crypto transactions commercially are regulated under MiCA. Record-keeping obligations and compliance controls apply, and transfer service providers must align with the EU’s Travel Rule requirements (the obligation to include originator and beneficiary information when transferring crypto-assets above defined thresholds, designed to support AML tracing).

Area 14: Significant Stablecoin Activities

Large ART and EMT issuers may be classified as significant under MiCA if they exceed defined thresholds: over 10 million holders or a market capitalization exceeding 5 billion euros. Significant issuers face enhanced supervision directly from the EBA rather than their national competent authority, stricter liquidity requirements, more frequent reporting obligations, and the possibility of supervisory intervention on issuance volumes if financial stability concerns arise.

What MiCA Does Not Cover: The Regulatory Frontier

Understanding which crypto activities are covered under MiCA regulation requires equal clarity on what sits outside its perimeter. Three areas currently occupy grey zones that businesses and their legal advisors must navigate carefully.

DeFi: The Decentralization Question

MiCA does not apply to fully decentralized protocols (blockchain-based systems that operate through autonomous smart contracts without any identifiable central operator, intermediary, or controlling entity). This exclusion is intentional. Regulation requires an identifiable legal entity to bear obligations. Where no such entity exists, MiCA cannot attach.

However, the definition of “fully decentralized” remains one of the most contested legal questions in EU digital asset law. Many protocols described as decentralized retain identifiable teams, foundations, governance token holders with voting control, or upgrade mechanisms that make true decentralization a matter of degree rather than an absolute condition. Regulators are unlikely to accept a formal claim of decentralization at face value where the substance of the activity includes identifiable operators exercising meaningful control.

This is the substance over form rule (the regulatory principle that the legal treatment of an activity is determined by what it actually does in practice, not by how it is labelled or structured on paper). If a protocol functions like a trading platform, custody service, or exchange, EU regulators may treat it as one regardless of whether it calls itself decentralized. ESMA has flagged DeFi classification as a priority area in its MiCA implementation roadmap.

NFTs: Unique Assets and the Fractionalization Risk

NFTs (Non-Fungible Tokens, unique digital assets that represent ownership of a specific item or piece of content and are not interchangeable with each other) are generally excluded from MiCA’s scope because their uniqueness distinguishes them from the fungible (interchangeable) assets MiCA was designed to regulate. However, two scenarios bring NFTs back within the regulatory perimeter:

- Large series issuance: NFTs issued in large collections where the tokens are functionally interchangeable despite being technically unique may be treated as fungible and therefore subject to MiCA.

- Fractionalized NFTs: When NFTs are divided into fractional ownership interests that are sold to multiple investors, the fractional interests may qualify as ARTs or financial instruments, triggering MiCA or MiFID II obligations.

Lending and Borrowing: The MiCA 1.0 Gap

Crypto lending and borrowing protocols represent a significant gap in MiCA’s current version. The regulation does not comprehensively address platforms that accept crypto deposits and issue loans, whether through centralized or decentralized mechanisms. This gap is widely acknowledged by European regulators and is expected to be addressed in future legislative reviews commonly referred to as MiCA 2.0. Until that framework materializes, lending platforms must navigate a patchwork of national regulations, existing consumer protection law, and AML requirements without a dedicated EU-level regime.

MiCA vs. MiFID II: Which Framework Applies?

The boundary between MiCA and MiFID II (Markets in Financial Instruments Directive, the EU’s existing framework governing investment services for financial instruments) is one of the most practically important classification questions for digital asset businesses. Understanding which crypto activities are covered under MiCA regulation versus MiFID II requires applying the financial instrument test to the underlying asset. ESMA has published specific guidance on the MiCA and MiFID II boundary to assist firms in making this determination correctly.

The key test is whether the underlying crypto-asset qualifies as a financial instrument under MiFID II. Security tokens (digital tokens that represent ownership rights in a company, a share of profits, or other investment returns, and therefore function like traditional financial securities) fall under MiFID II, not MiCA. The EU’s regulatory design was deliberate: assets that already have an equivalent in traditional finance remain within the existing regulatory framework. Only assets that are genuinely novel to the digital asset space fall under MiCA.

Where the classification is ambiguous, the substance over form principle applies again. An asset structured to avoid security token classification while providing investment returns and ownership-like rights will likely be evaluated on its economic substance rather than its technical label.

| Dimension | MiCA | MiFID II |

|---|---|---|

| Asset Type | Crypto-assets not qualifying as financial instruments | Financial instruments including security tokens |

| Authorization Type | CASP license | Investment firm authorization |

| Passporting | Yes, across all 27 EU member states | Yes, across all 27 EU member states |

| Classification Test | Residual: applies when MiFID II does not | Applies to financial instruments as defined in Annex I |

Institutional Evaluation Criteria

Institutions assessing their MiCA compliance posture examine several interconnected questions. Which crypto activities are covered under MiCA regulation for their specific business model? Which national competent authority is the appropriate home regulator? Can the passporting mechanism support multi-market operations from a single authorization? How does the ART or EMT classification affect reserve and redemption obligations? And do any current activities fall into the DeFi, NFT, or lending grey zones that may attract regulatory scrutiny under the substance over form principle? These questions must be answered in sequence, not in isolation.

For broader compliance architecture context:

- Key Objectives of the MiCA Regulatory Framework

- Why Compliance Matters in Tokenized Finance

- Regulatory Risks in Tokenized Asset Platforms Explained

- How Regulation Improves Transparency in Tokenized Finance

Frequently Asked Questions

Which crypto activities are covered under MiCA regulation?

Which crypto activities are covered under MiCA regulation spans two parent categories: crypto-asset issuance and crypto-asset service provision. Issuance covers ARTs, EMTs, and public offerings of other crypto-assets including admission to trading. Service provision covers ten regulated activities: operation of trading platforms, custody and administration, exchange for fiat, exchange for other crypto-assets, execution of orders, placing, portfolio management, advisory services, transfer services, and significant stablecoin activities.

Does MiCA apply to DeFi protocols?

MiCA explicitly excludes fully decentralized protocols with no identifiable operator. However, the substance over form rule means that protocols with identifiable controlling entities, governance token holders, or upgrade mechanisms may be treated as regulated service providers regardless of how they are labelled.

What is the difference between an ART and an EMT under MiCA?

An ART references a basket of multiple assets and requires direct national authorization. An EMT is pegged to a single fiat currency and must be issued by an authorized e-money institution. Both prohibit interest payments and face enhanced EBA supervision above defined significance thresholds.

What is CASP passporting under MiCA?

CASP passporting allows a firm authorized as a Crypto-Asset Service Provider in one EU member state to provide regulated crypto services across all 27 EU countries without requiring separate national licenses. This is one of MiCA’s most strategically significant features for businesses scaling across EU markets.

Are NFTs covered under MiCA?

Unique NFTs are generally excluded from MiCA. However, NFTs issued in large series that function like fungible assets, or NFTs that are fractionalized into investor ownership interests, may fall within MiCA or MiFID II scope depending on their economic characteristics.

Is crypto lending regulated under MiCA?

Not comprehensively. Crypto lending and borrowing represents a gap in MiCA’s current version. It is expected to be addressed in future legislative reviews. Until then, lending platforms must navigate existing national regulations and AML requirements without a dedicated EU-level framework.

Conclusion

Which crypto activities are covered under MiCA regulation is one of the most consequential questions in EU digital asset compliance today. The answer spans fourteen structured areas across both crypto-asset issuance and the full range of professional crypto services, while deliberately excluding fully decentralized systems, unique NFTs, and crypto lending from the current regulatory perimeter. Understanding where that boundary sits is not merely a compliance exercise. It is a strategic prerequisite for any business building within EU digital asset markets.

The three most actionable insights from this article are these. First, the ART and EMT distinction determines reserve obligations, redemption rights, and supervisory relationships from the earliest stages of issuance design, making correct classification essential before any token is issued. Second, CASP passporting is the single most compelling structural advantage of operating under MiCA, enabling a firm authorized in one member state to scale across all 27 EU markets from a single regulatory base. Third, the substance over form principle means that which crypto activities are covered under MiCA regulation is determined not by how an activity is labelled but by what it actually does in practice, a standard that applies with particular force to DeFi protocols and fractionalized NFTs that may function like regulated services regardless of their technical architecture.

For related compliance and regulatory framework coverage:

- What Is MiCA Regulation in Crypto?

- How MiCA Regulation Affects Tokenized Assets

- MiCA Regulation vs National Crypto Regulations in Europe

- Key Objectives of the MiCA Regulatory Framework

- What Is VARA: Dubai’s Virtual Asset Regulatory Authority Explained

- Regulations and Compliance Hub

Educational Disclaimer

This article is provided for informational and educational purposes only. It does not constitute legal, financial, or investment advice. Regulatory requirements, authorization obligations, and supervisory frameworks vary by jurisdiction and are subject to change. Professional legal consultation should be sought before making any compliance or licensing decisions.

Last updated: March 2026

{kind=link}